Facebook EMEA’s ninth COVID LIVE Webinar was delivered on Wednesday 27th April. Below are the key insights from the session:

1) Create, don’t wait for demand

With the Rightmove app seeing its biggest ever day of traffic at the end of May and people queuing up for hours outside Ikea, there is clearly some pent up demand. However, we shouldn’t take this to mean that there will a sudden rush to the high street. Google footfall data from Germany suggests that consumers will return gradually.

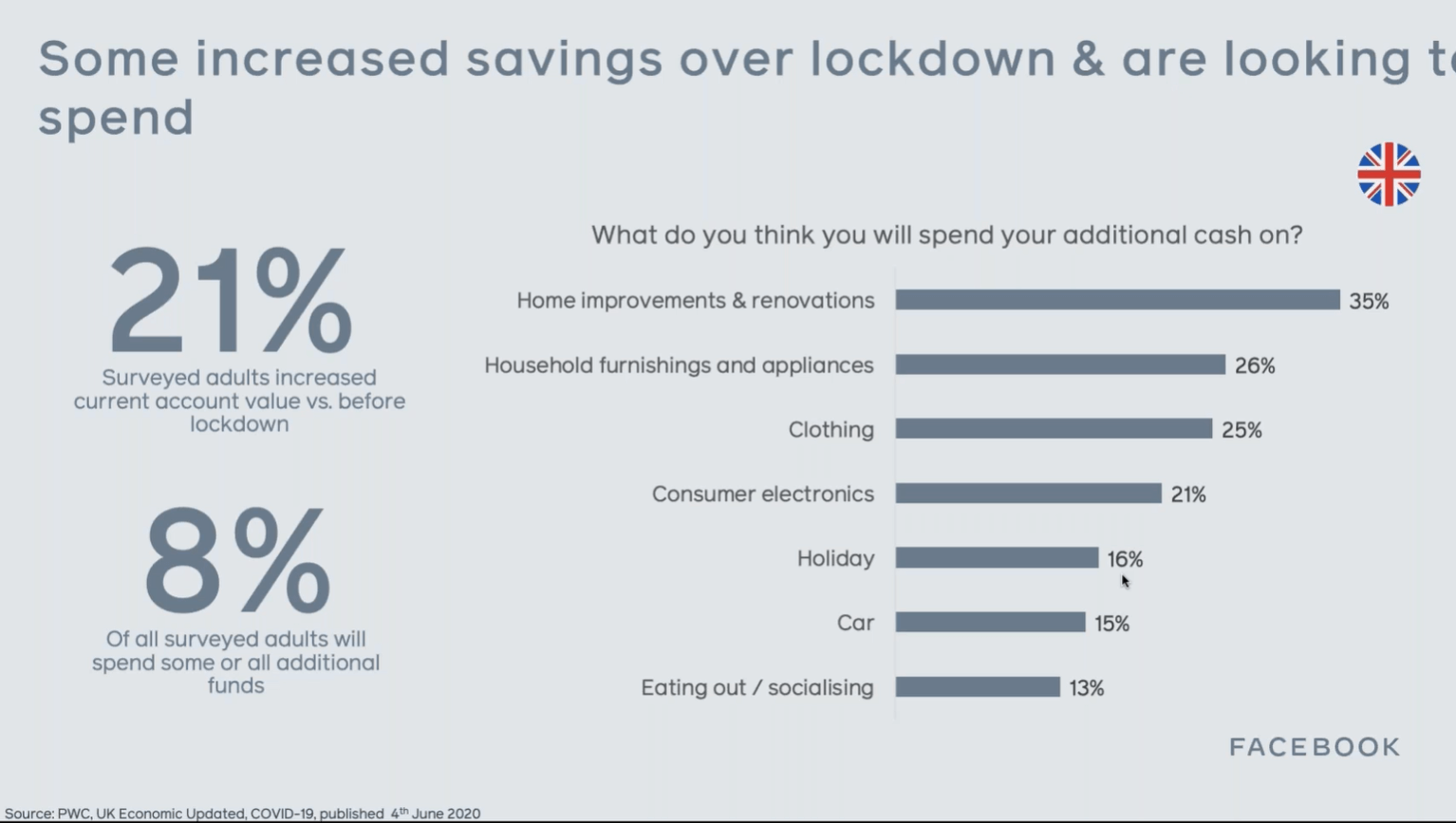

Throughout the lockdown, many consumers have delayed large purchases, and some of these people will now be re-entering the market with money to burn. This is obviously a minority, but 21% of adults have more money in their current account than before lockdown, and 8% are now looking to spend some or all of these additional funds. Interestingly, despite the fact (or perhaps because of the fact) that we’ve all been cooped up in our houses over the past few months, these people are still looking to spend their additional money on purchases for the home.

However, the majority of consumers will not be rushing back to shops looking to spend big, and 35% of Brits now say that they will now be waiting for products to be on promotion before purchasing. This is number is up from 27% at the end of April.

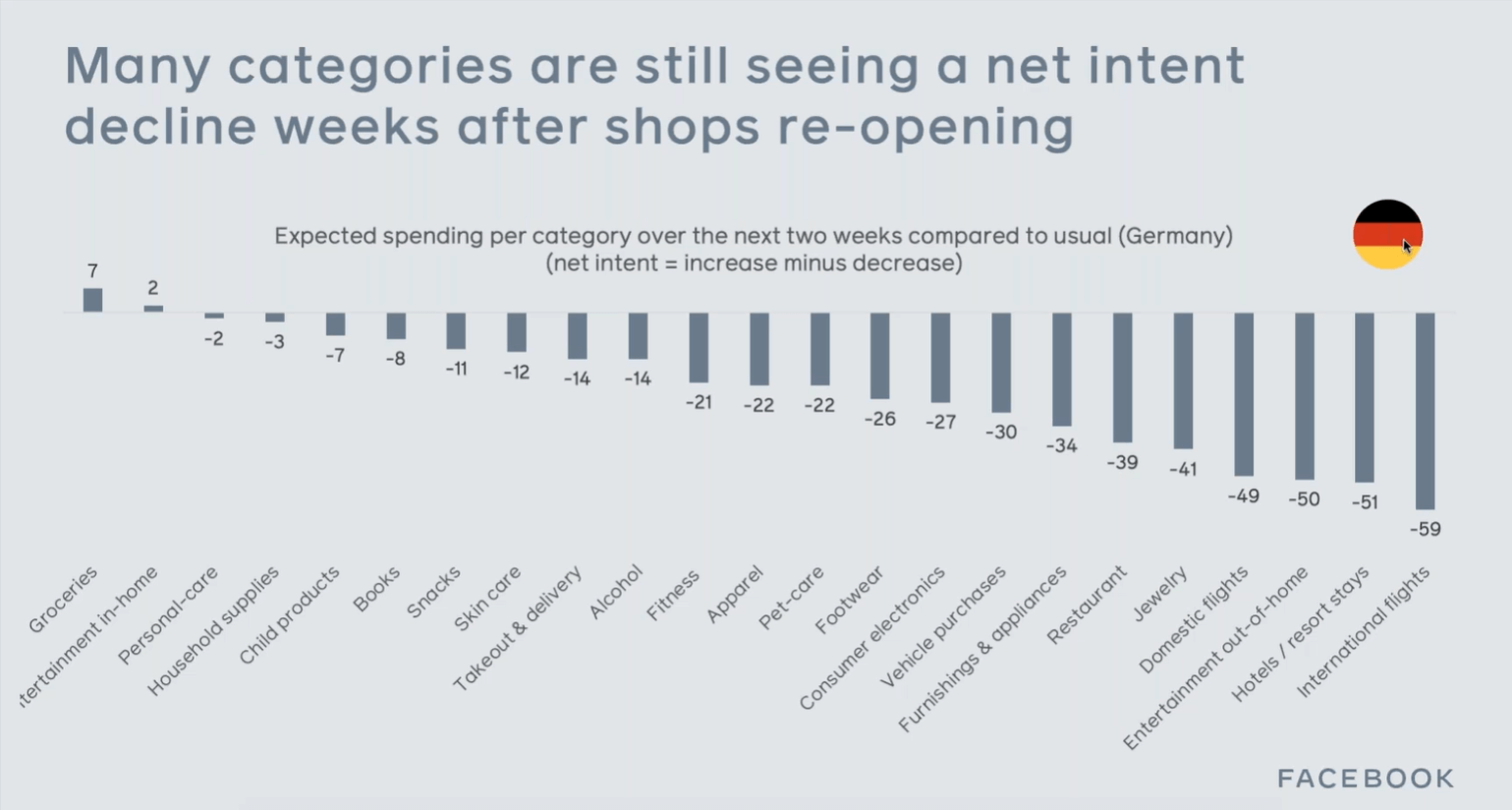

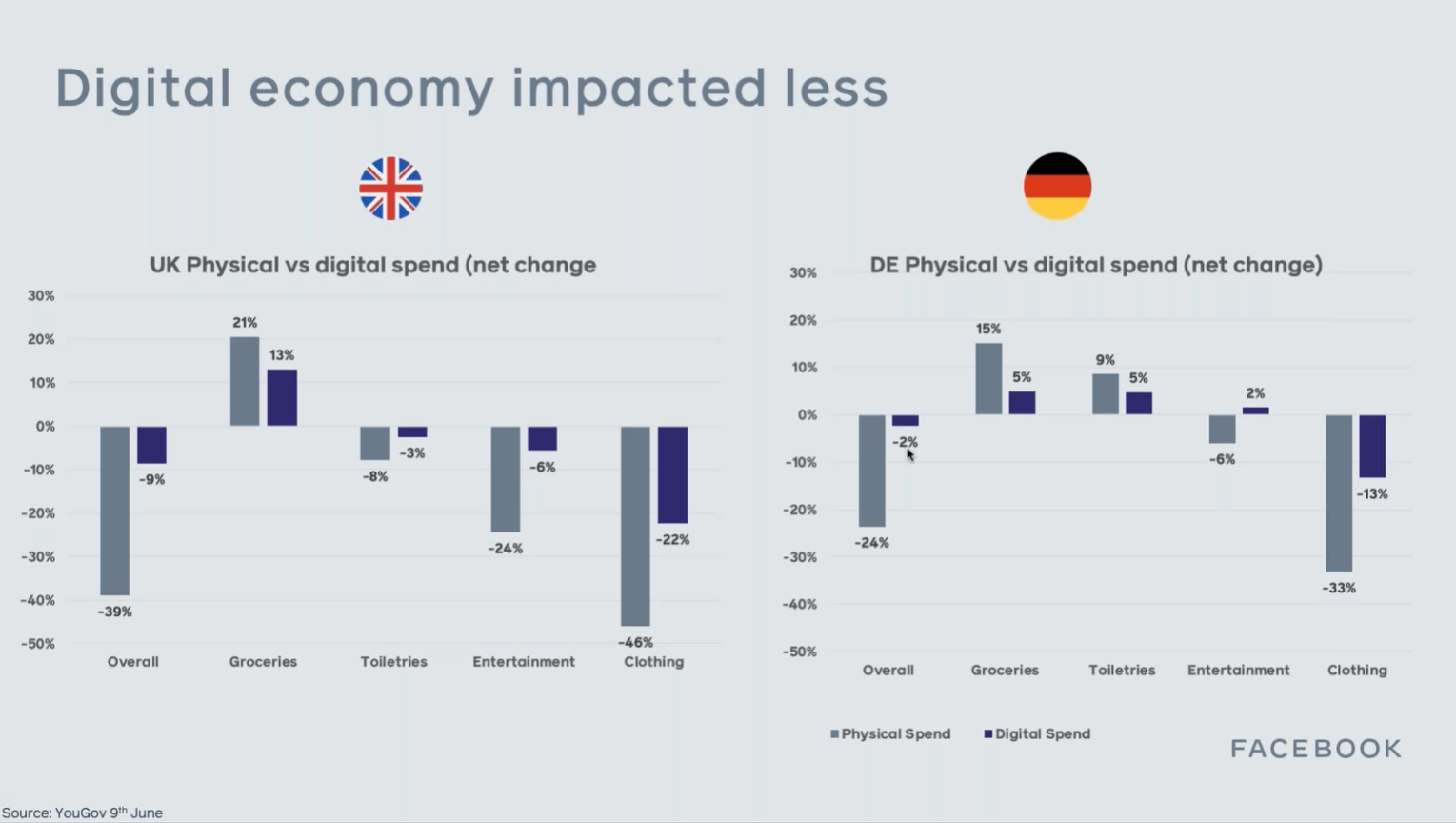

Data from Germany shows that net intent is still down across the vast majority of categories, with groceries and in-home entertainment the only ones showing more intent and travel and luxury categories suffering heavily.

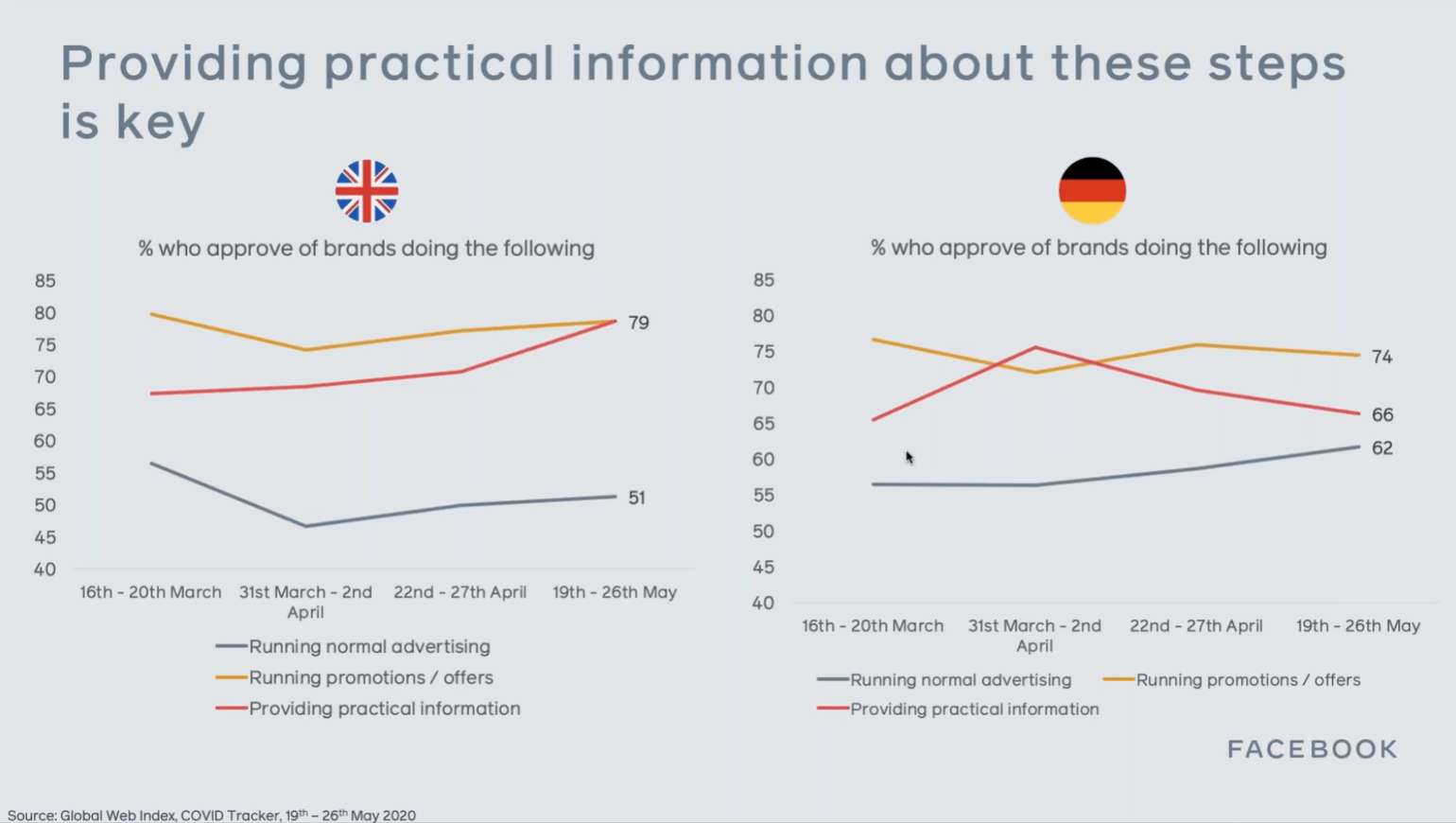

However, when it comes to bringing shoppers back into the fold, safety still trumps price. According to GWI, 93% of UK adults believe new safety features will be important in any public space. For retailers, actively responding to these demands will be critical in the coming months, as consumers will only want to spend time and money in environments where they feel safe. The most important safety factors for consumers are shown below:

After implementing these safety procedures, brands need to make them known to their customers. The UK consumer has a growing desire for practical information from brands, and this has now even caught up with the desire for promotions and offers.

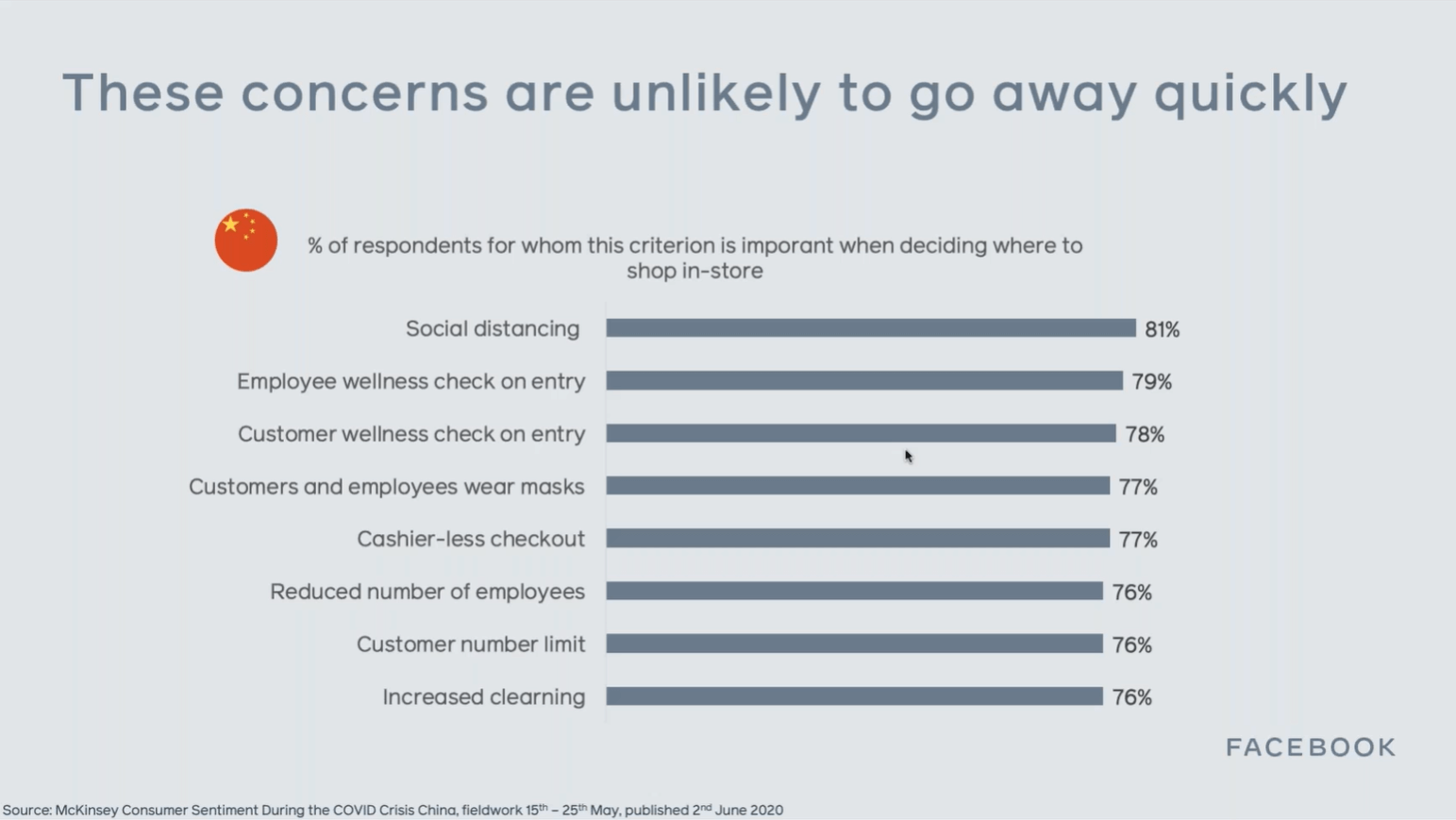

Taking learnings from China, it seems that these concerns over safety will be persistent for many months to come, with 81% of Chinese respondents saying that social-distancing is still an important factor when deciding where to shop in-store.

However, Chinese retailers have not simply been waiting for this anxiety to blow over. Thousands of brands actually came together to create demand by putting on a new retail festival, Shanghai 5/5. This festival brought in $2 billion dollars of revenue, and shows that by coming together to provide a truly exciting event for consumers, brands create demand.

2) People don’t go shopping, they go buying

Shops are re-opening in the UK, but ‘shopping’ may never truly concern. The concept of a day out at a shopping centre, aimlessly browsing, stopping for coffee-breaks and meals, now seems wholly anachronistic.

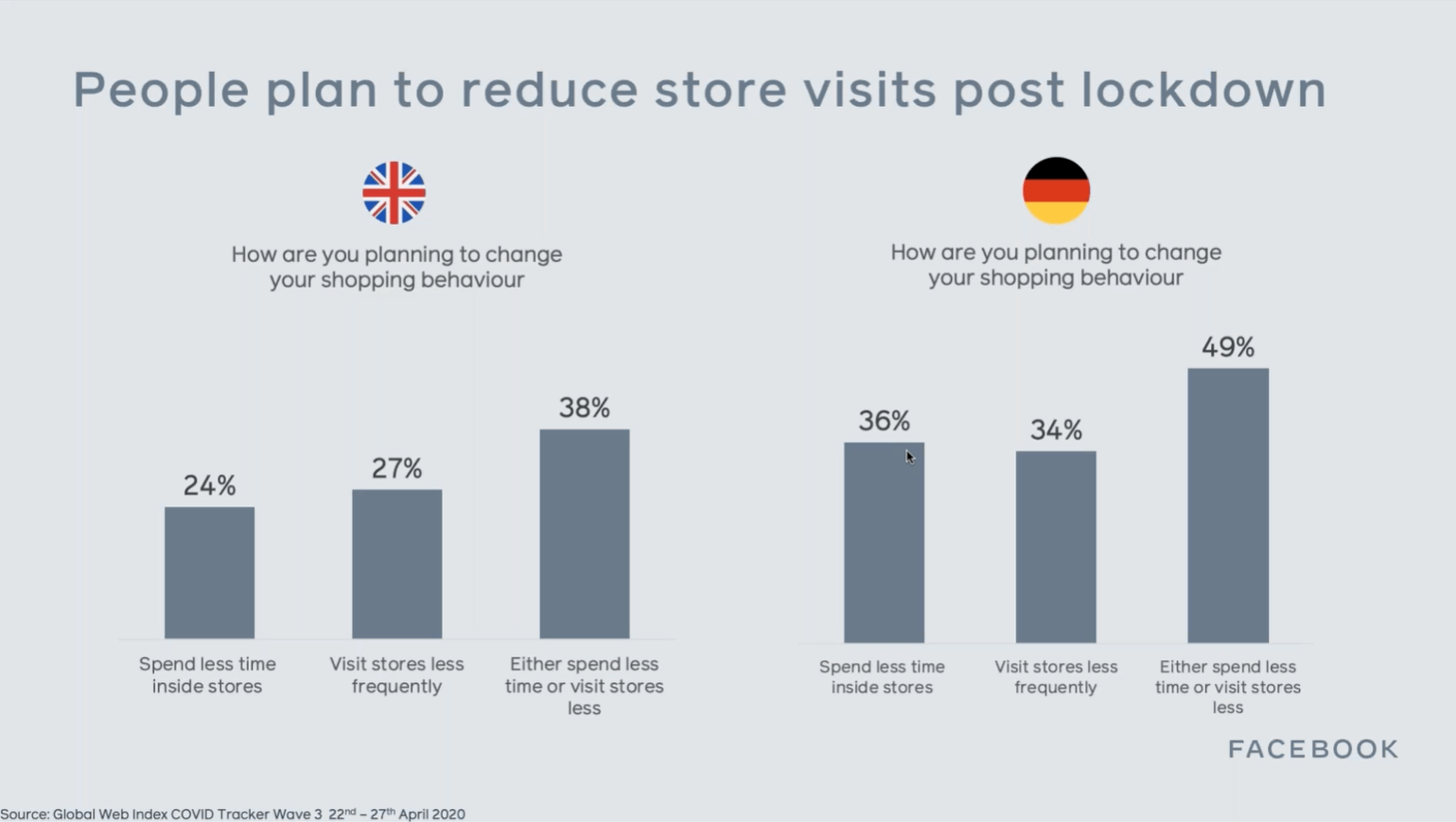

Brits are now planning on shopping less frequently, and for a shorter duration on each outing.

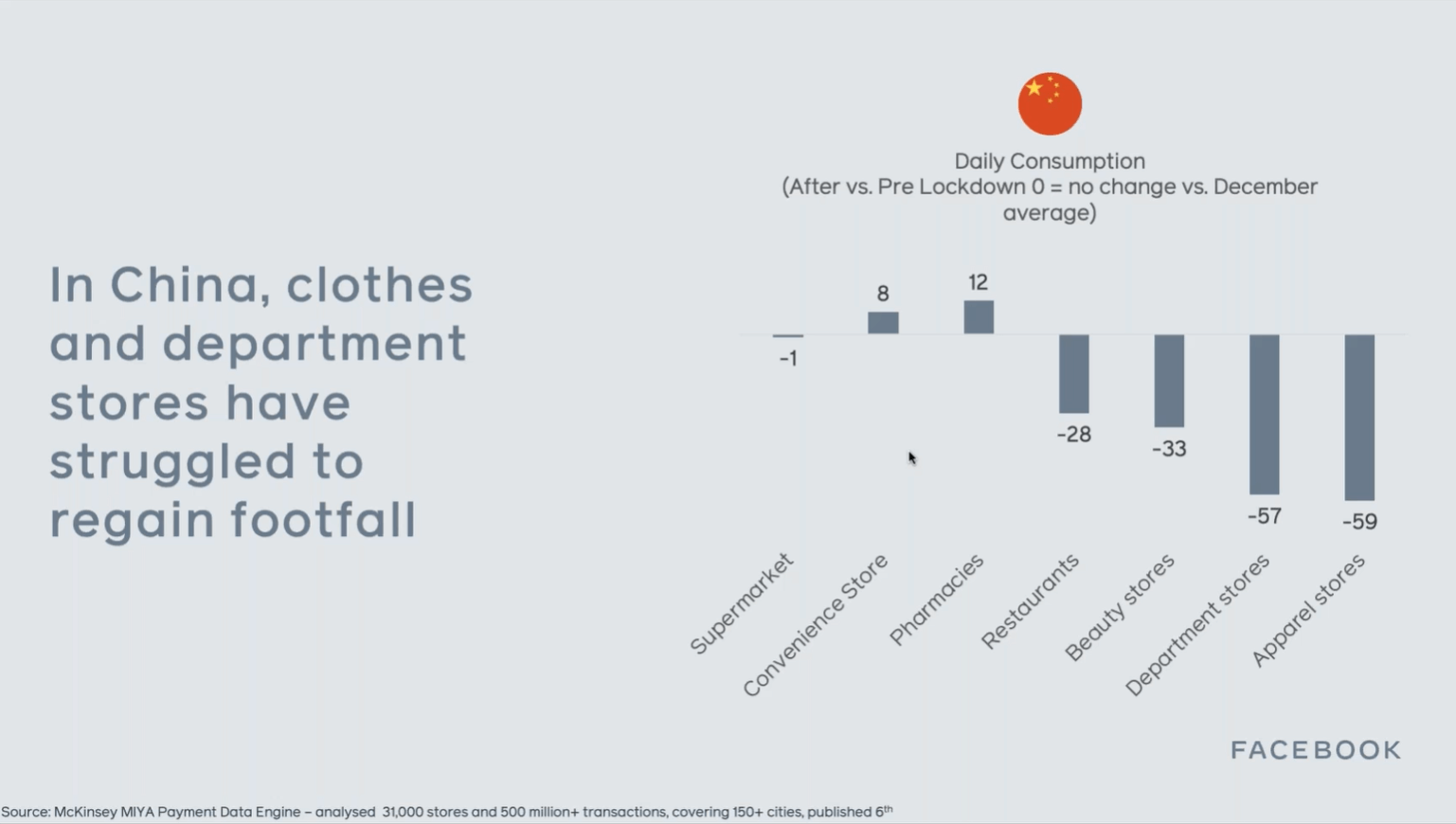

As shopping becomes a less recreational and more utilitarian activity, in-store discovery is likely to suffer. Clothes shops and the already beleaguered department store are likely to be the hardest hit by this behaviour shift, and both are still down almost 60% in China.

The other loser across retail is likely to be the shopping malls, which are currently showing a net intent of -21% in the UK.

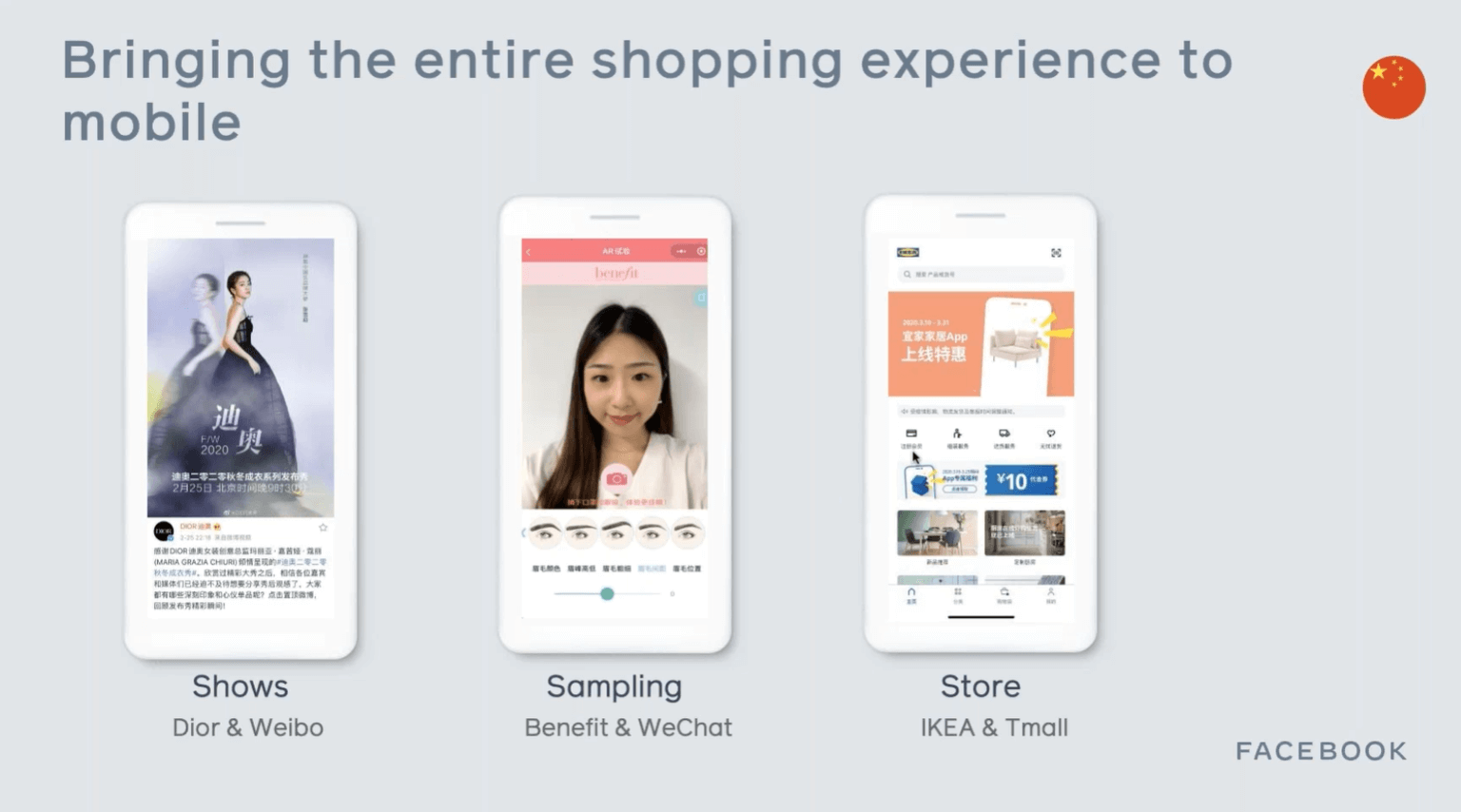

Again, looking to China for inspiration, we see brands bringing the entire shopping experience onto mobile, whether that is through streaming fashion shows, providing AR sampling, or opening up new digital retail space as IKEA have done by partnering with Chinese Amazon-equivalent TMALL.

As consumers continue to avoid busy spaces, now is a time for brands to take a step back and consider the most cost-effective way of acquiring consumers. Will brick-and-mortar stores still provide value? Is now the time to unsilo budgets and test putting money that would be spent on retail rent into digital?

3) Prepare to be a pandemic-proof brand

“Now is the time for preparation, not celebration”

Dr Hans Kluge, WHO Director for Europe, 8th June 2020

Sadly, Hans is right. Now is not the time to celebrate. There is a very real threat of a second peak this Autumn and brands need to think about how they can find opportunity in a time of crisis, laying down the type of foundations for growth that Alibaba did during the Sars crisis in 03-04. Rather than trying to wait it out, they need to be focusing on becoming pandemic-proof.

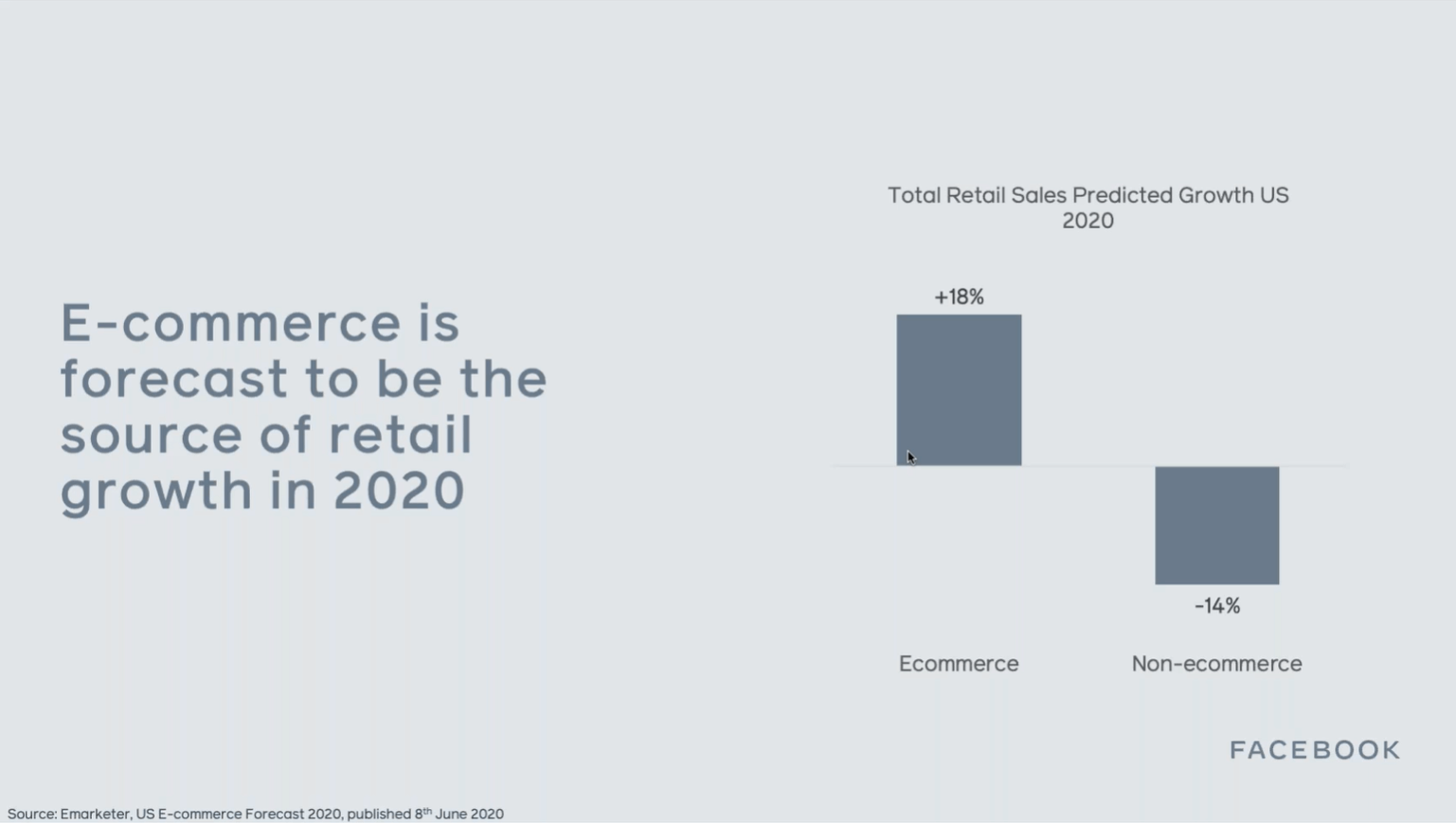

More and more shopping is being done online and brands need to prepare for this trend to continue.

As consumers continue to avoid physical shops, any retail growth will come from digital and brands will be forced to recalibrate how they reach consumers.

As more consumers shop online, the way that brands collect and use first-party data will become even more crucial than it is today. Those who can provide personalised, frictionless experiences will emerge as the victors.

For established brands such as Heinz, ABinBev and Nestle, who recently dipped their toes into selling D2C online, the main hurdle will be the last mile, and Nestle have solved this ingeniously by teaming up with Deliveroo.

As we look forward into the new normal, it seems increasingly clear that a pandemic-proof brand must be digital, flexible and co-operative.

Thanks to the Facebook EMEA team for another informative session. This was the last in the series, but we are looking forward to what comes next!

For more COVID-19 insights, read our summary of last week’s COVID LIVE, or download our whitepaper on The Effects of COVID-19 on Search Behaviour