Facebook EMEA’s seventh COVID LIVE Webinar was delivered on Wednesday 13th April. Below are the key insights from the session:

1) The recessionary mindset

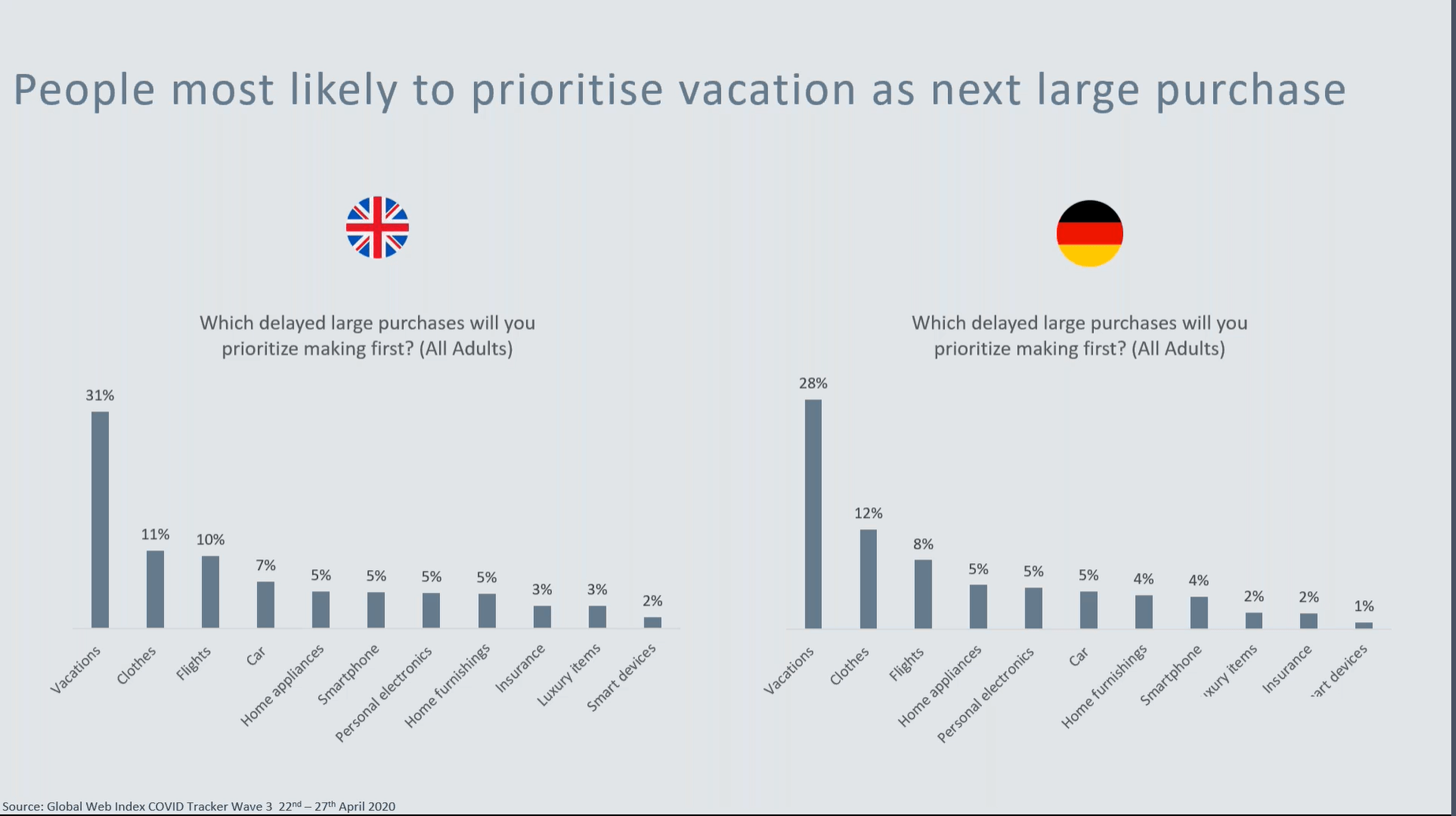

The pandemic caused 69% of UK consumers to delay a large purchase, as lockdown is lifted and these large purchase-delayers are now clearly prioritising booking holidays:

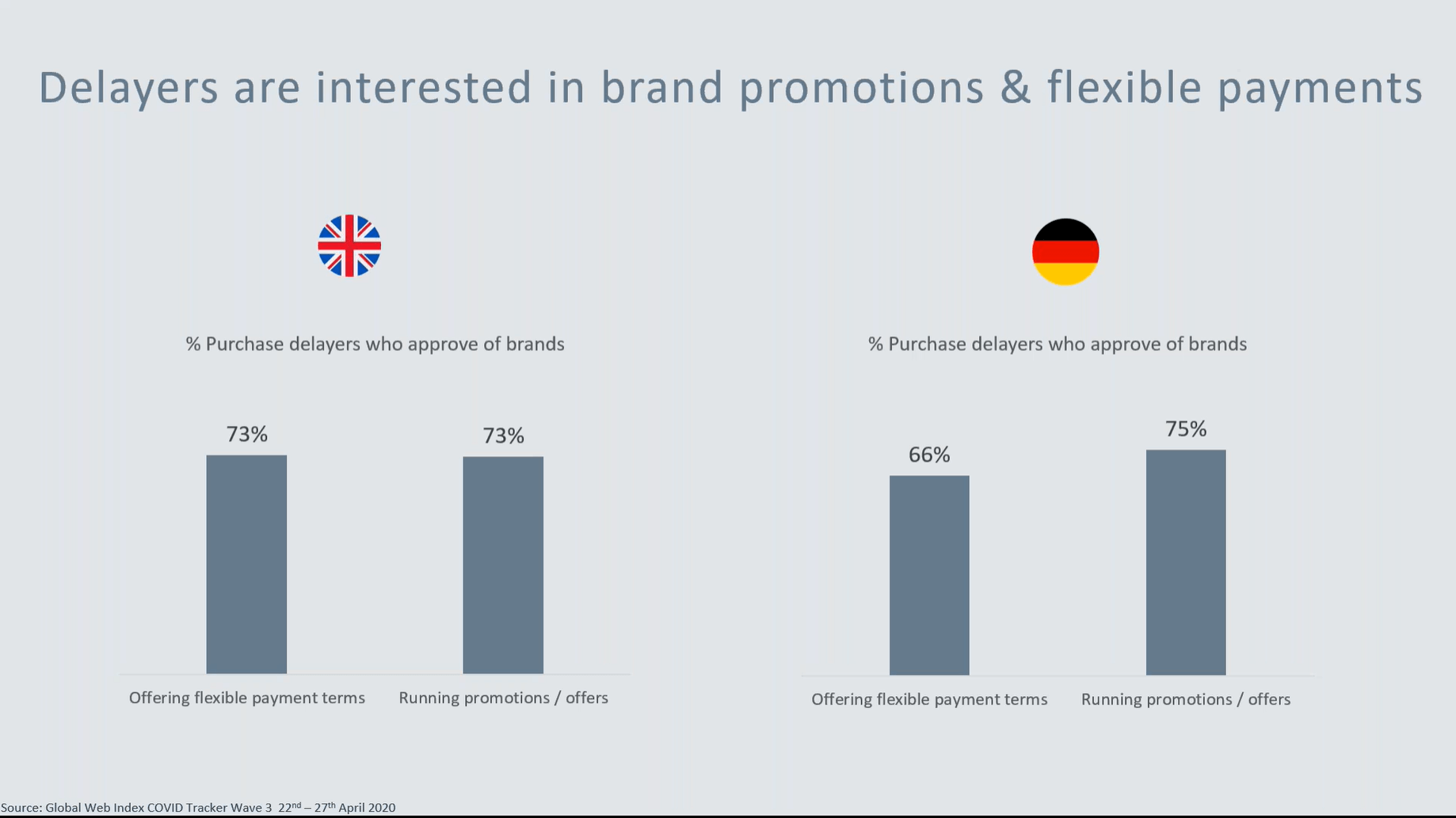

However, the mindsets that people take when purchasing have now become ‘recessionary’, meaning that consumers want more for less. GWI data shows that 73% of UK purchase delayers approve of brands running promotions/ offers, and the same percentage want brands to offer flexible payment terms.

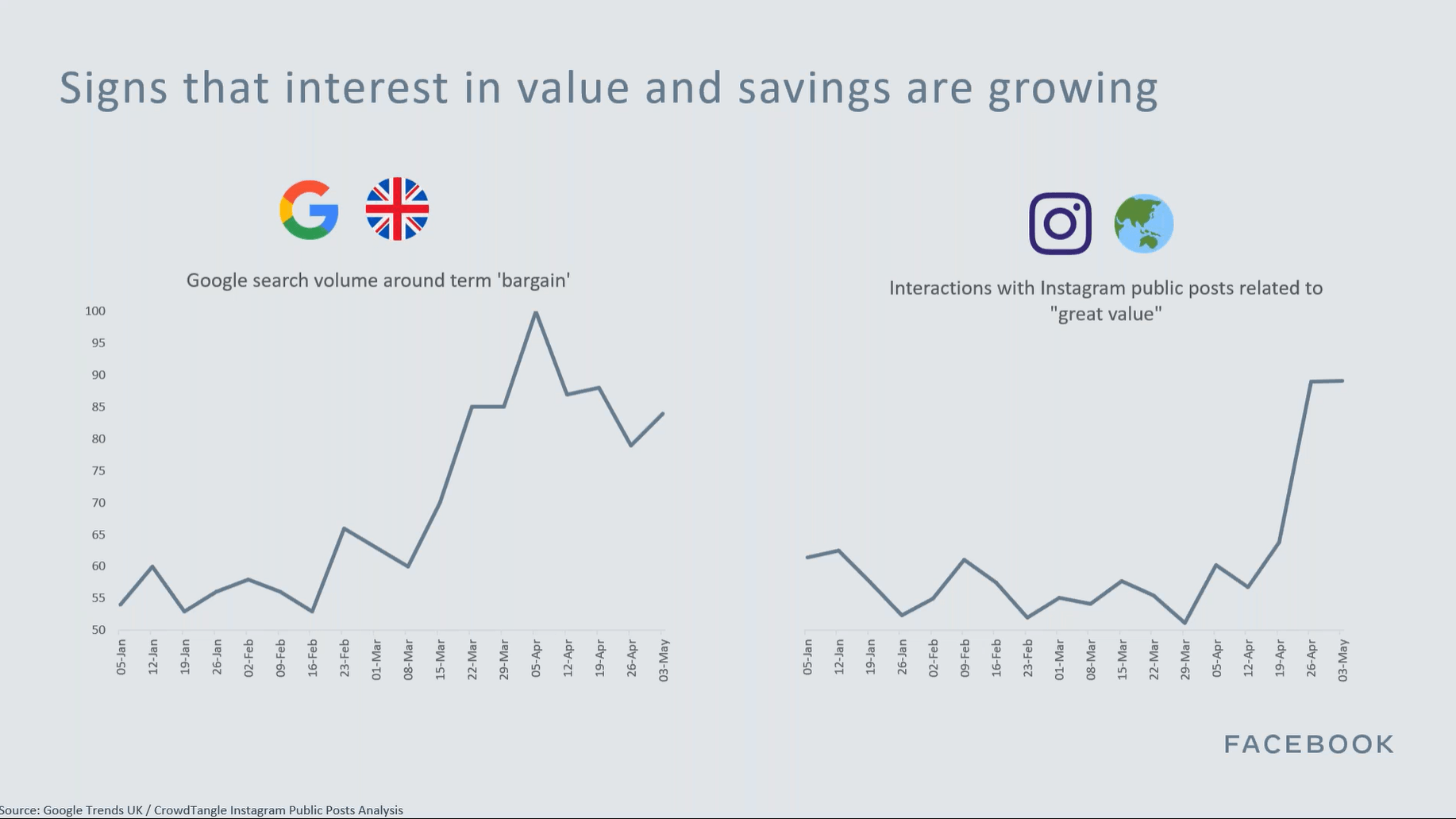

People have begun actively seeking out lower prices, and Google search volumes around ‘bargain’ and interactions on Instagram with posts related to ‘great value’ have both seen large increases in recent weeks.

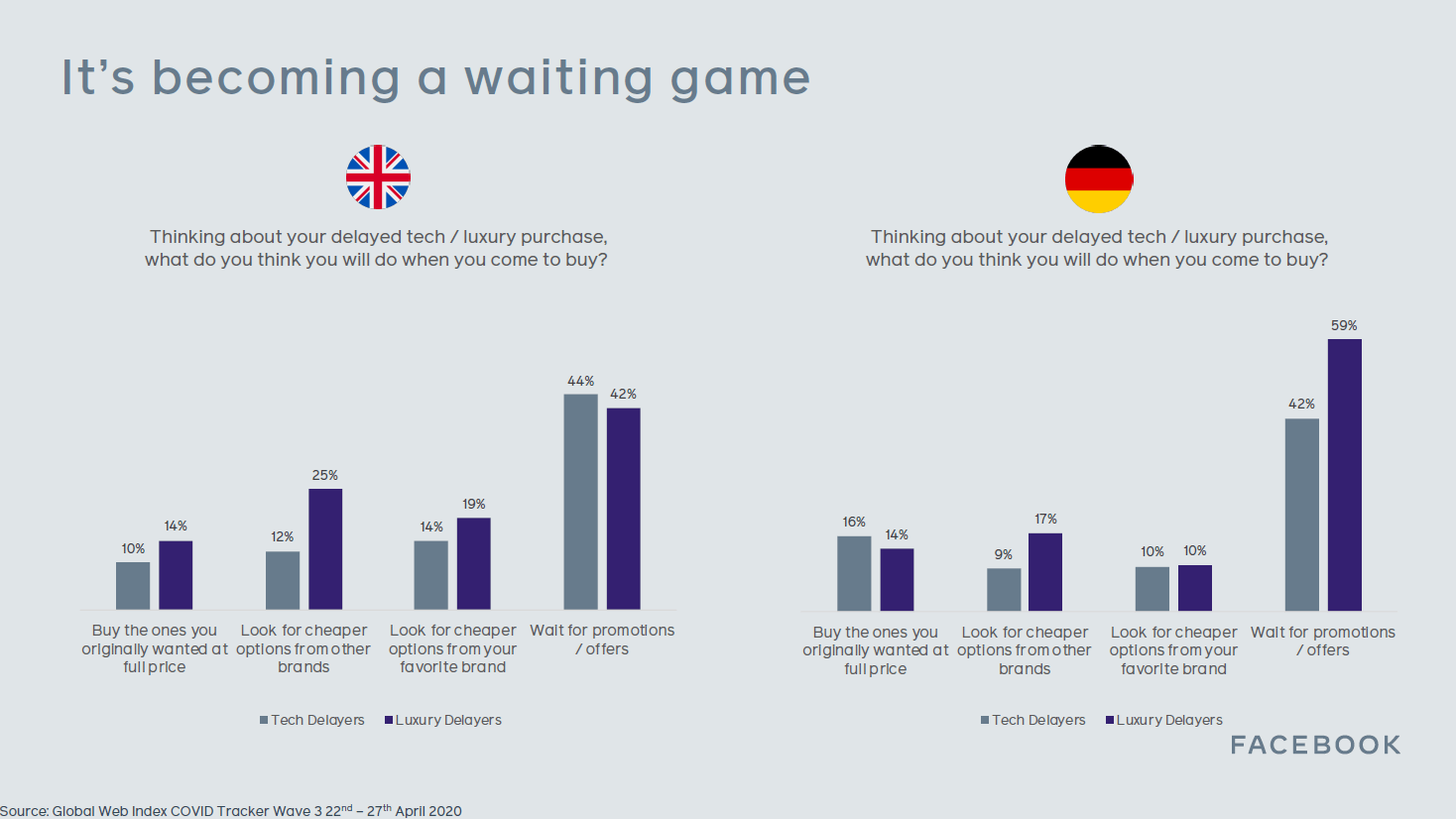

When consumers do get around to making the purchases that they have delayed, many will wait for a sale or look for a cheaper option – only 1 in 10 say they will buy the same item they were going to purchase originally at the same price. Consumers are willing to play a waiting game.

Another way for brands to approach this problem is to add value to their products, rather than decreasing cost. A good example of this is beauty company Glossier launching a new handcream and giving the first 10,000 units away to healthcare workers, then collaborating with artists to create content surrounding the product and even creating its own AR filter so you can see it in your own home. By elevating a handcream to a cultural item, Glossier ensured demand despite the product’s high-price point.

Brands should be asking:

- How can we reframe our offer to better fit a more price-conscious world?

- How do we increase the desirability of our product to out-weigh price?

2) Safety over savings

Safety is an even bigger concern than savings, and consumers are not going to feel comfortable in busy shops for some time.

For brands, being able to measure and manage the business of physical locations and communicate to consumers willl become increasingly important. A great example of this is Lidl Ireland, who have rolled out a WhatsApp chatbot which allows consumers to find out when their local store will be least busy.

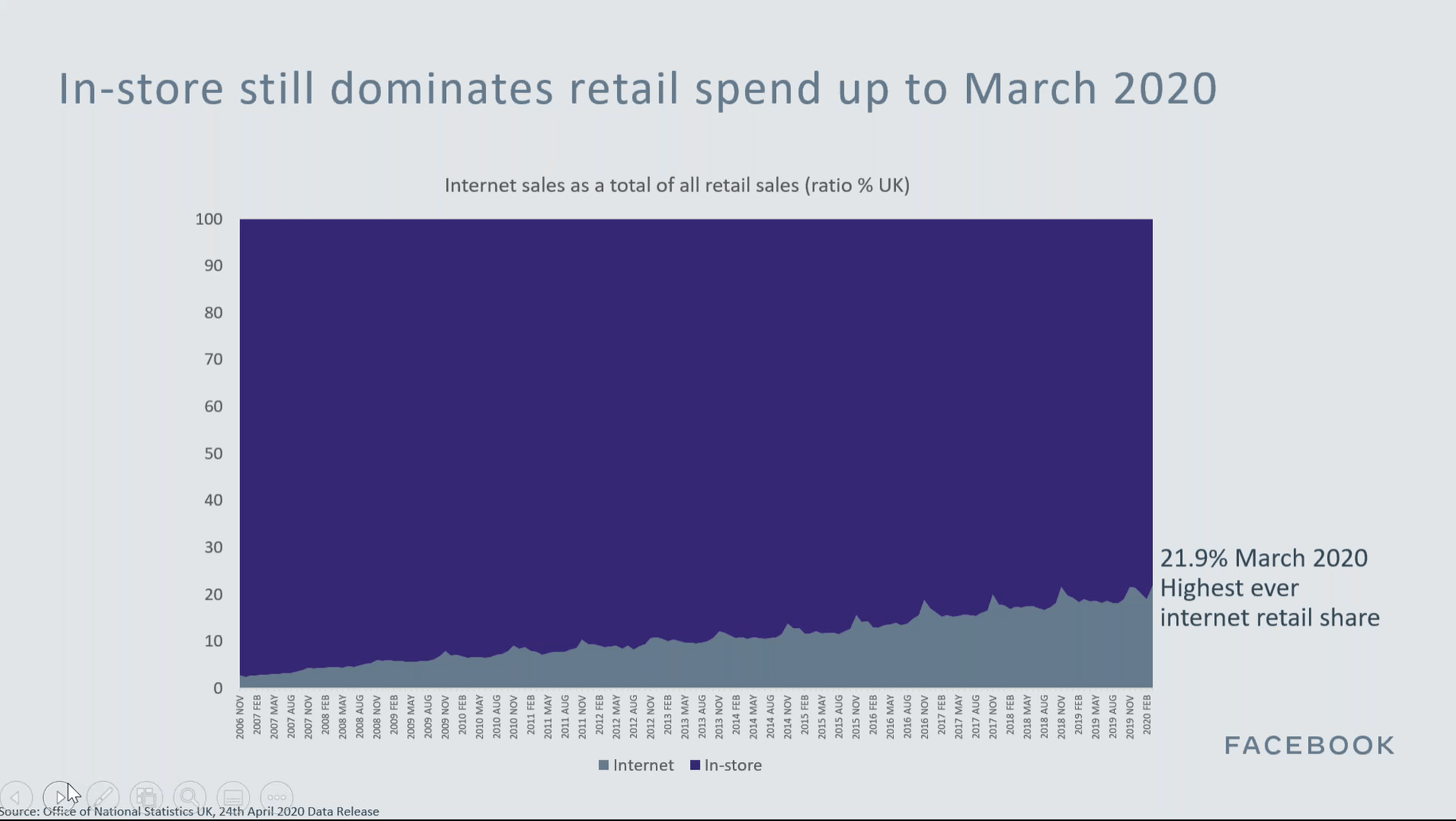

Working in Digital, its sometimes easy to forget that the vast majority of retail spend still happens in-store. This data from the ONS shows that March 2020 was the highest ever month for online, but it still only accounted for 21.9% of all sales:

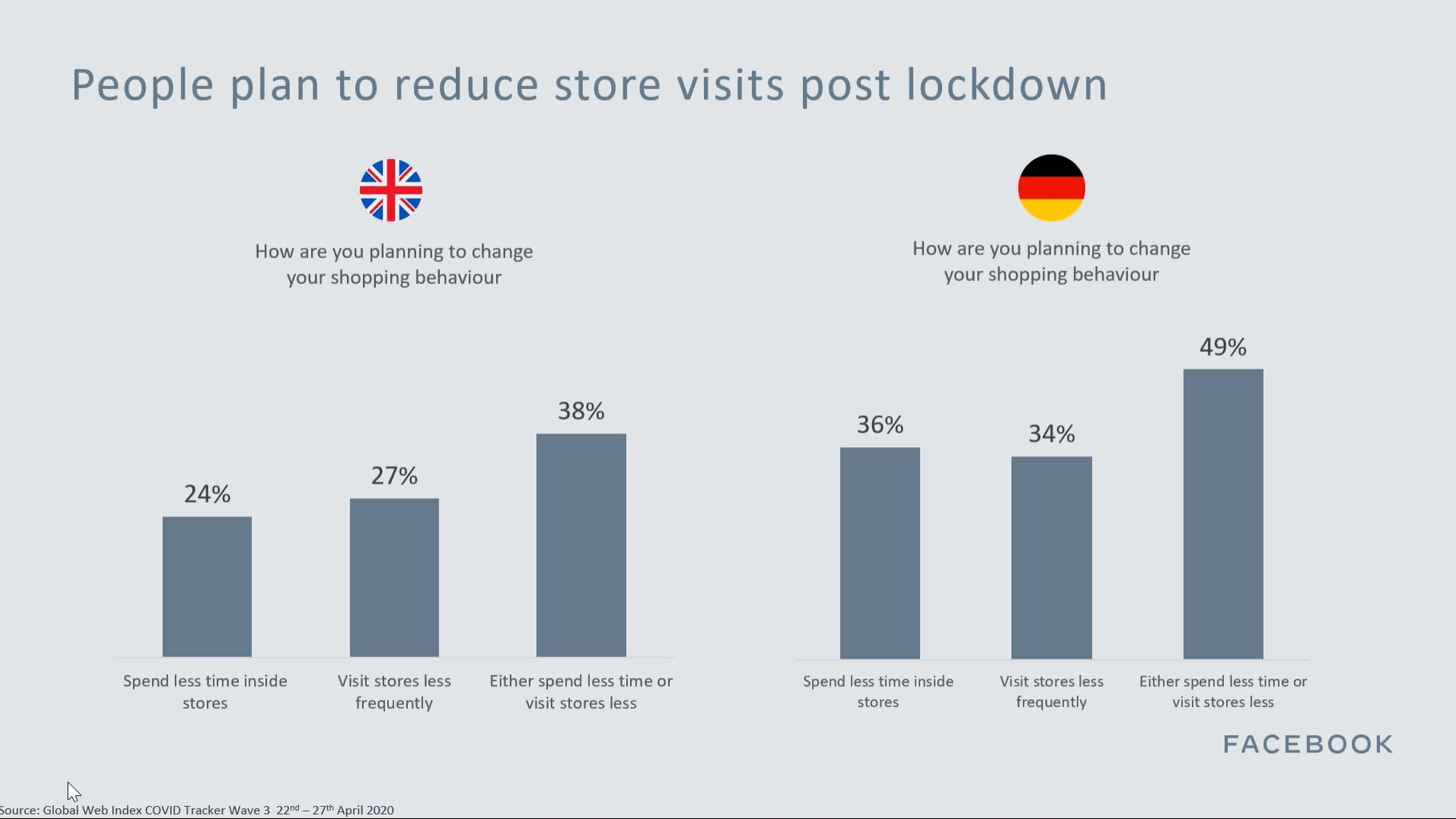

The ongoing uneasiness that people will feel in crowded indoor spaces is likely to accelerate this shift towards online retail, with 38% of Brits saying they will either spend less time inside stores or visit stores less frequently post lockdown.

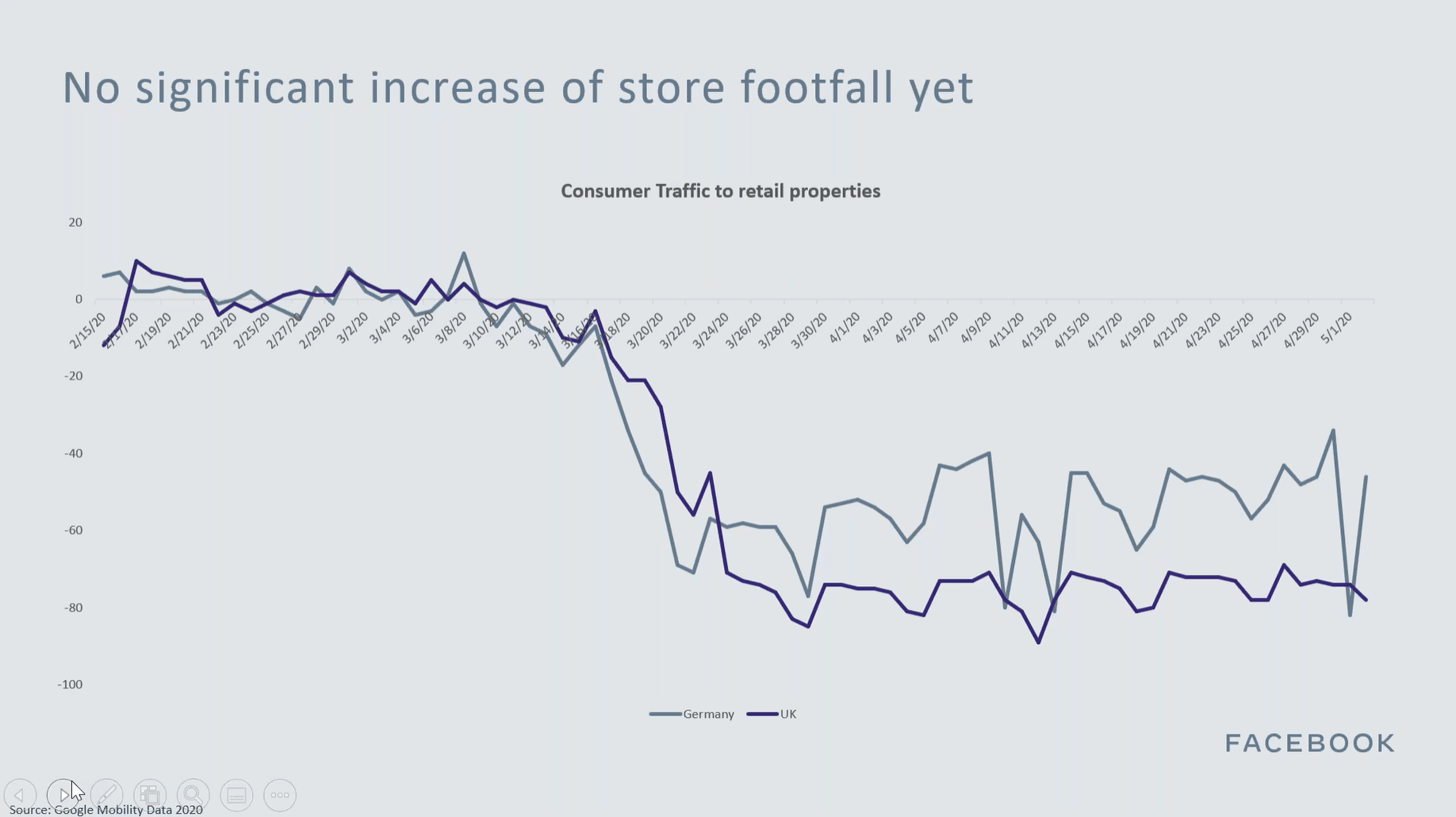

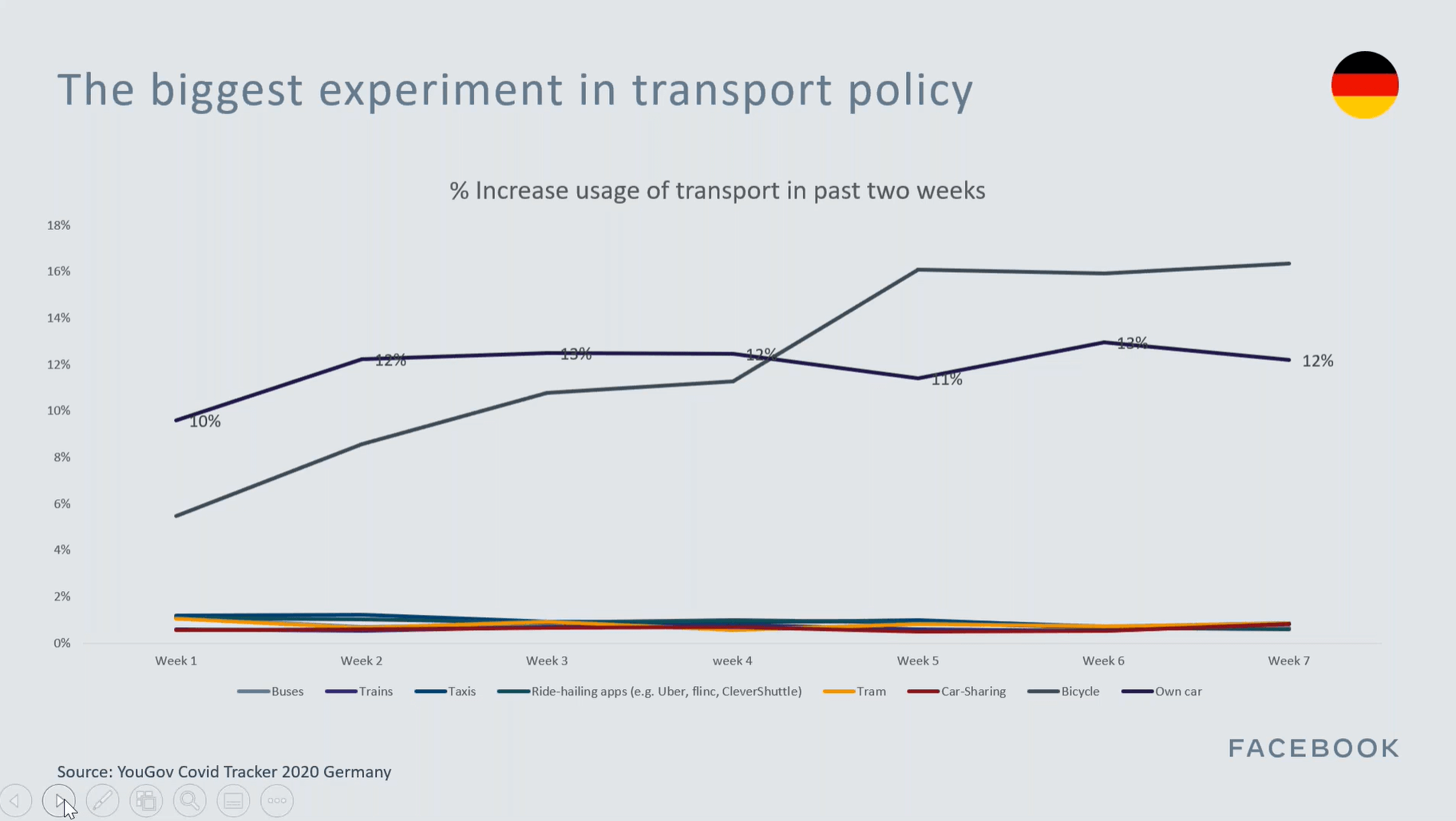

Google movement data from Germany, where lockdown has already been partially lifted, suggests that the return to physical retail will be slow. We shouldn’t expect the high-streets to be flooded with shoppers as soon as restrictions are lifted.

We are seeing more and more FMCG brands shift towards Ecommerce and Facebook are enabling brands to make the transition with formats such as Collaborative Ads (where brands collaborate with retailers) and Multi-Retailer ‘Add-to-cart’ Ads (where consumers can add products seen in ads on Facebook or Instagram directly to their online shopping cart at their chosen supermarket).

Brands should be asking:

- How can our brand become famous for helping people feel more comfortable in-store?

- What steps can we take to develop and simplify our ecommerce offering?

3) A catalyst to build a greener future

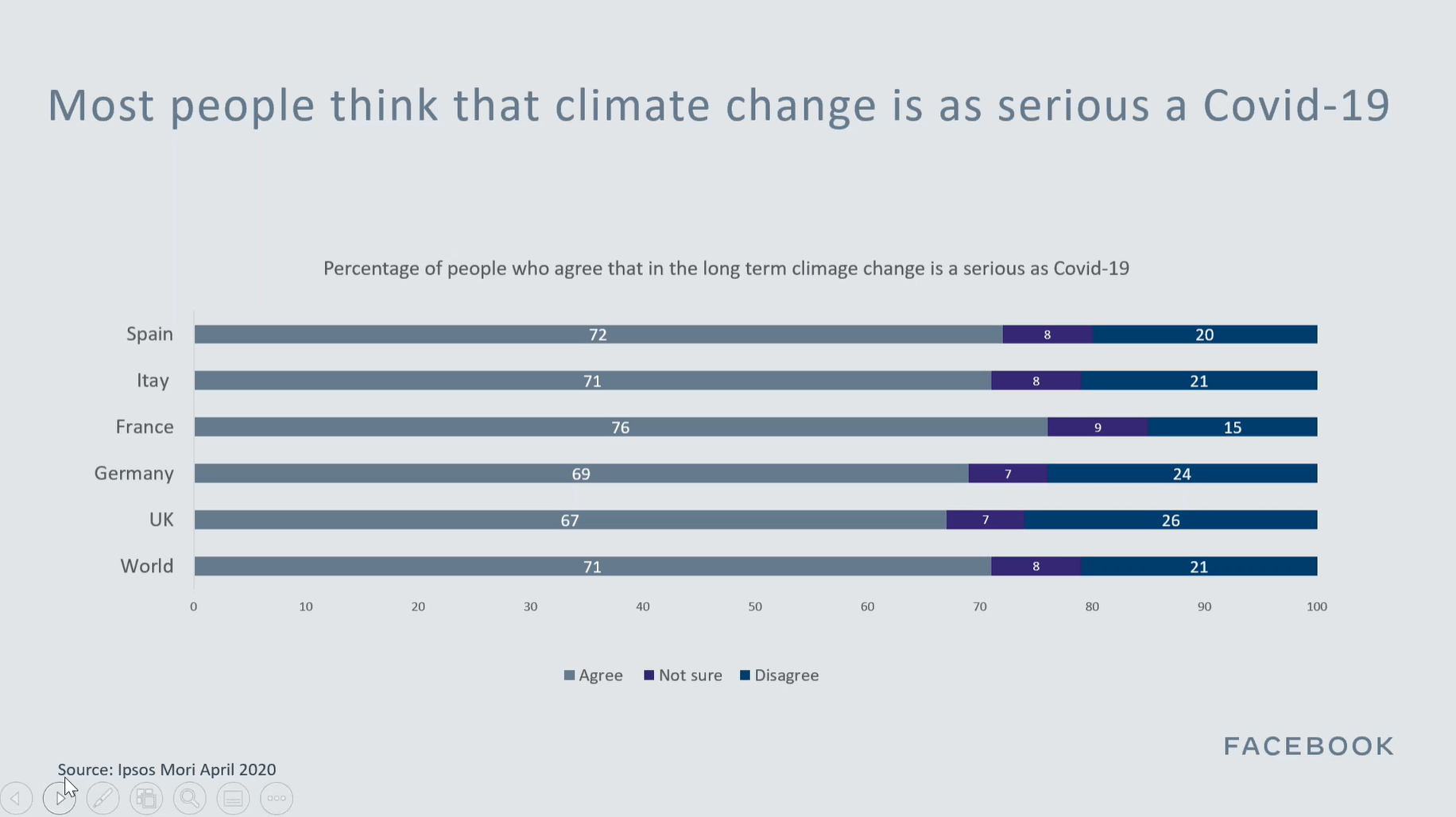

The other big crisis, which to a certain extent has been overshadowed by the immediacy of Covid-19, is of course climate change. Data from Ipsos Mori shows that 67% of Brits believe that it is as serious as Covid-19.

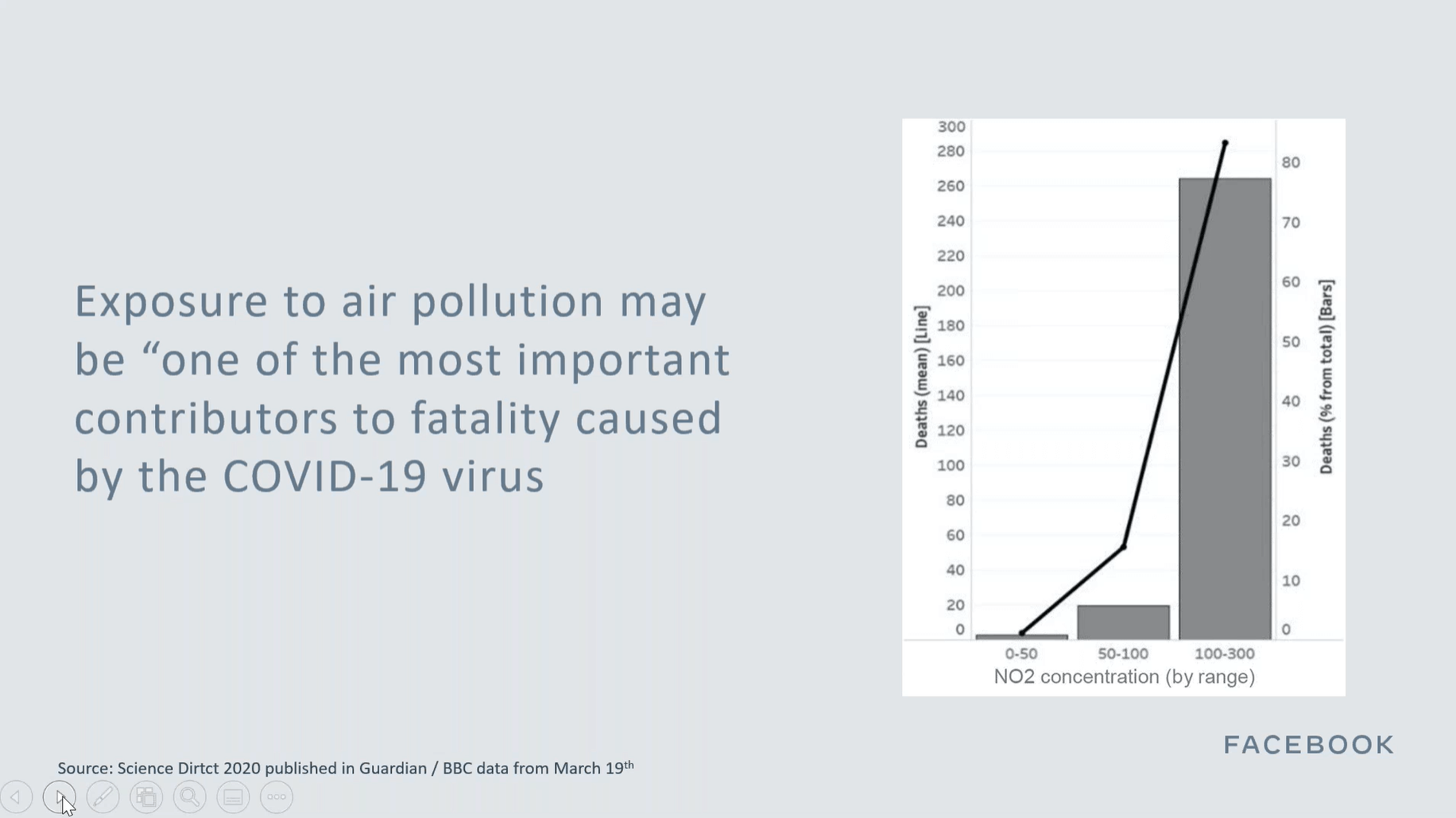

One of the positive effects of the pandemic has been a dramatic reductions in emissions, with NO2 pollution in London down 44% YoY. Some studies suggest that exposure to air pollution is one of the major factors in COVID-19 fatalities, with over 70% of fatalities occurring in areas with high air pollution.

In cities worldwide, the pandemic is causing people to experiment with their modes of transport. Bicycles have seen surge in popularity, with Halfords reporting a 20% rise in sales.

As people avoid public transport they are also doing more journeys in their own car. Amongst drivers there is a clear trend towards trying to be more eco-conscious, with 4/10 of the top searched cars in the past month being electric.

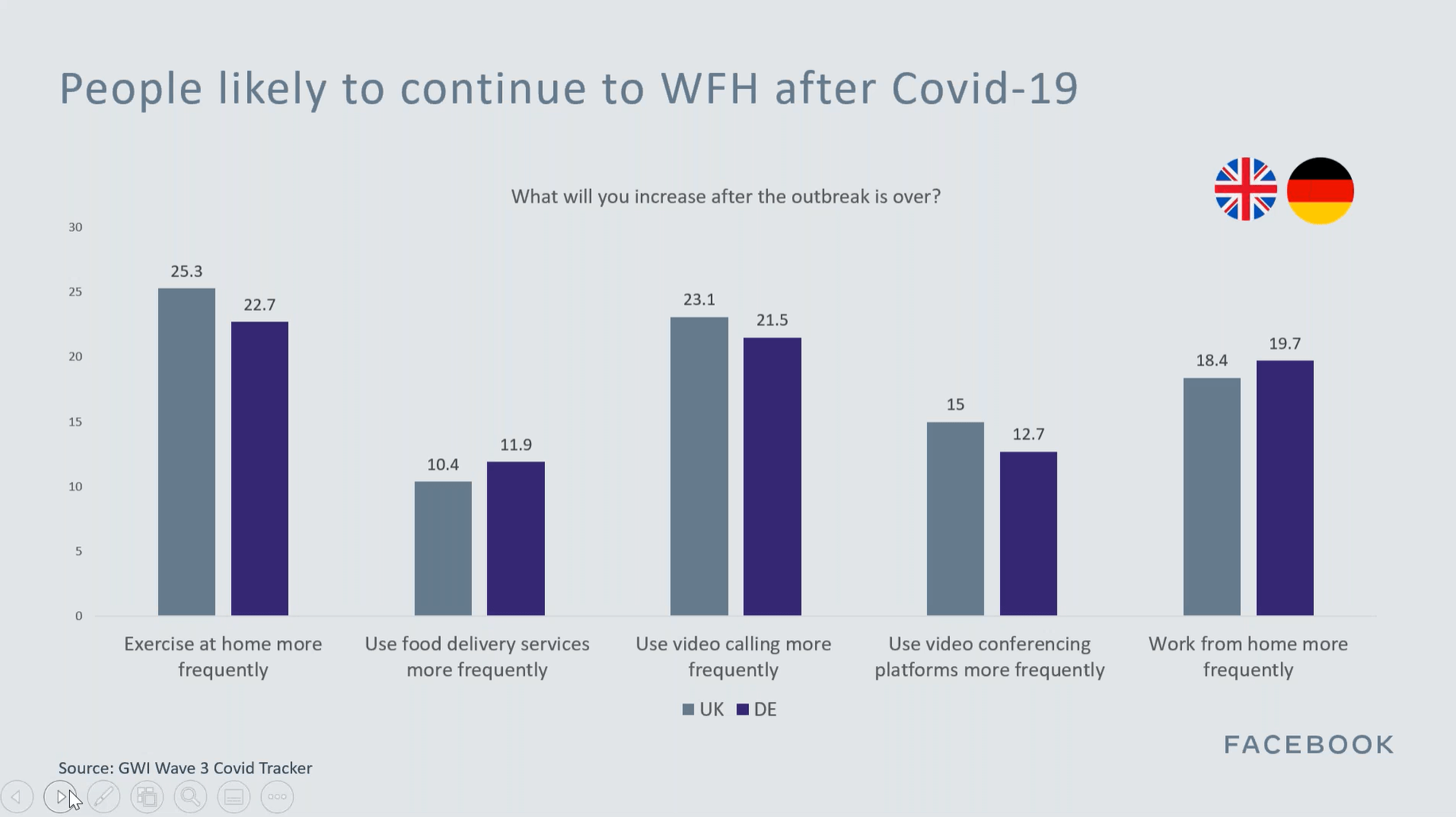

However, it is likely that the biggest shift in transport that we will see after the lockdown ends will not be commuters choosing different modes of getting around, it will be commuters deciding not to commute.

For many people the WFH experiment is proving to be a success, and the best thing about it is not having to waste a part of your day on an expensive, unhygienic and stressful commute. For many businesses, employees’ willingness to work from home will provide a lifeline in the coming recession.

The positives of WFH are now well documented. A study by Stanford University, looking at 16,000 employee Chinese travel agency Ctrip, found that when they switched to WFH:

- There was a 13% productivity increase, with more minutes worked and more work done per minute.

- Employee attrition decreased by 50%

- Company saved saved nearly US$2,000 per employee on rent by reducing their office footprint.

Martin Sorrell sees this as a big advantage for agencies, saying that; “For digital natives, working from home is part of their work …We’re already cutting our leases…we see a distinctive change in the pattern of working, and our people are saying that they prefer working from home”.

However, not everyone can work from home. Rather than being the ‘great leveller’ that some people thought it would be, the pandemic has affected people of different socioeconomic backgrounds in markedly different ways. YouGov’s Covid tracker from 8-11th May shows that 63% of ABC1 workers can always or sometimes work from home, compared to only 28% of C2DE workers.

Brands should be asking:

- Will working remotely remain?

- What does this mean for cities, suburbs, transport, companies, employees and marketing?

Thanks to the Facebook EMEA team for another informative session. We will be back in two weeks time with our next write up.

For more COVID-19 insights, read our summary of last week’s COVID LIVE, or download our whitepaper on The Effects of COVID-19 on Search Behaviour