The third installation of Facebook’s weekly webinar series saw Peter Buckley and Andy Childs take us through the latest trends in how consumers and brands are reacting to COVID-19, focusing on data from the UK and Germany. The insights were broken down into three key trends:

1) Moving away from passive consumption

Content consumption continues to grow, but the rate of growth is slowing down.

It seems people have become saturated with news, and fatigue is beginning to set in. However, it is worth noting that this data is from before it was announced that Boris Johnson was going into intensive care, a shocking development which will have led to another jump in UK news consumption.

The huge increase in content consumption has coincided well with the Disney plus launch, and Amazon and Netflix have reported rises in viewing of ~40%, leading them to take the decision to move from HD to SD to increase bandwidth.

The growth has been seen across AVOD and SVOD, with Twitch reporting 3 billion hours watched in Q1!

However, despite all this passive consumption, people are becoming increasingly bored, illustrated by this 918% increase in volume of posts including the word ‘bored’ on Instagram.

This boredom is leading us to go beyond passive consumption and start trying to learn new skills, such as breadmaking. Ecommerce company Stackline have reported a 652% increase in sales of breadmakers in the US comparison with March last year. Weights are one of the other big winners, up 307% YoY.

Mobile game downloads are also reported to have grown 30% in March

As we move towards more active consumption, Instagram live provides an interactive platform for brands to connect with consumers.

We’ve seen influencer/comedian The Fat Jewish create his own gameshow on instagram complete with huge giveaways, collaborating with other celebrities such as Emily Ratajkowski to bring together their huge fan bases to promote his wine brand.

Brands need to be asking how they can actively engage with the millions with more time on their hands. What is your role as a brand at this time? Is it to entertain? To inform? To assist?

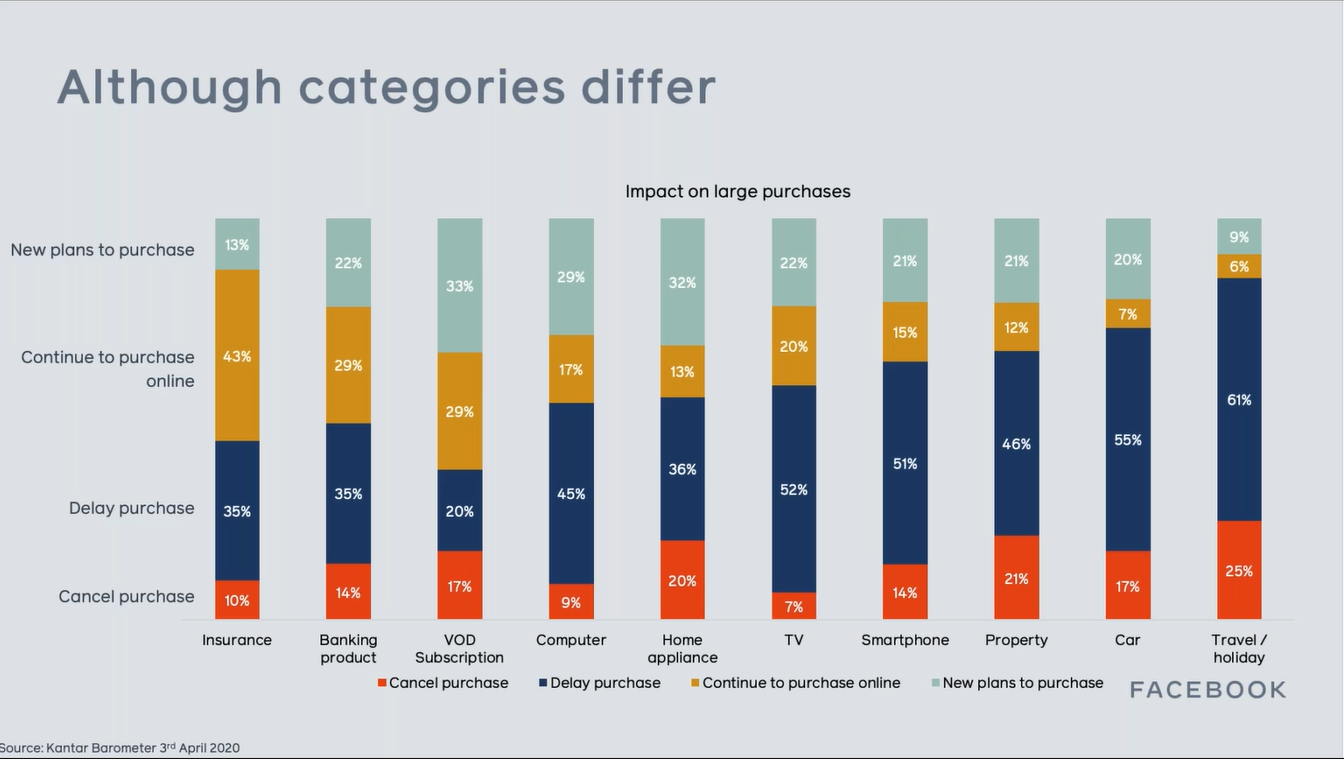

2) Most big purchases delayed, not cancelled

There has been an increase in the number of people who have delayed a large purchase, and this number is now at 76% in the UK.

However, most people are delaying, rather than cancelling.

Behaviour differs across categories. Across some, such as VOD and Home Appliances, many people are making new plans to purchase.

In travel 9% of people are making new plans, probably using spare time to start planning for 2021.

Those who are delaying tend to be doing so until the outbreak is over.

And it is becoming clearer than ever to people that we are in this for the long-run.

The Australian tourist board for example is encouraging potential visitors to look to the future. There is still opportunity for brands to play at the top of the funnel and inspire future trips.

The aesthetic of the creative here reflects a consumer desire to try to relax and be meditative, echoed in Spotify listening trends which have shown growth in ‘chill’, low-energy, acoustic playlists. For brands, tapping into the zeitgeist is pivotal, and the Australian tourist board have done that excellently.

3) We are entering the next phase

Fear is receding and boredom is increasing. Despite most health bodies suggesting that the crisis has not yet reached its peak in the UK, YouGov data shows the percentage of of people who are scared of catching Coronavirus is now decreasing.

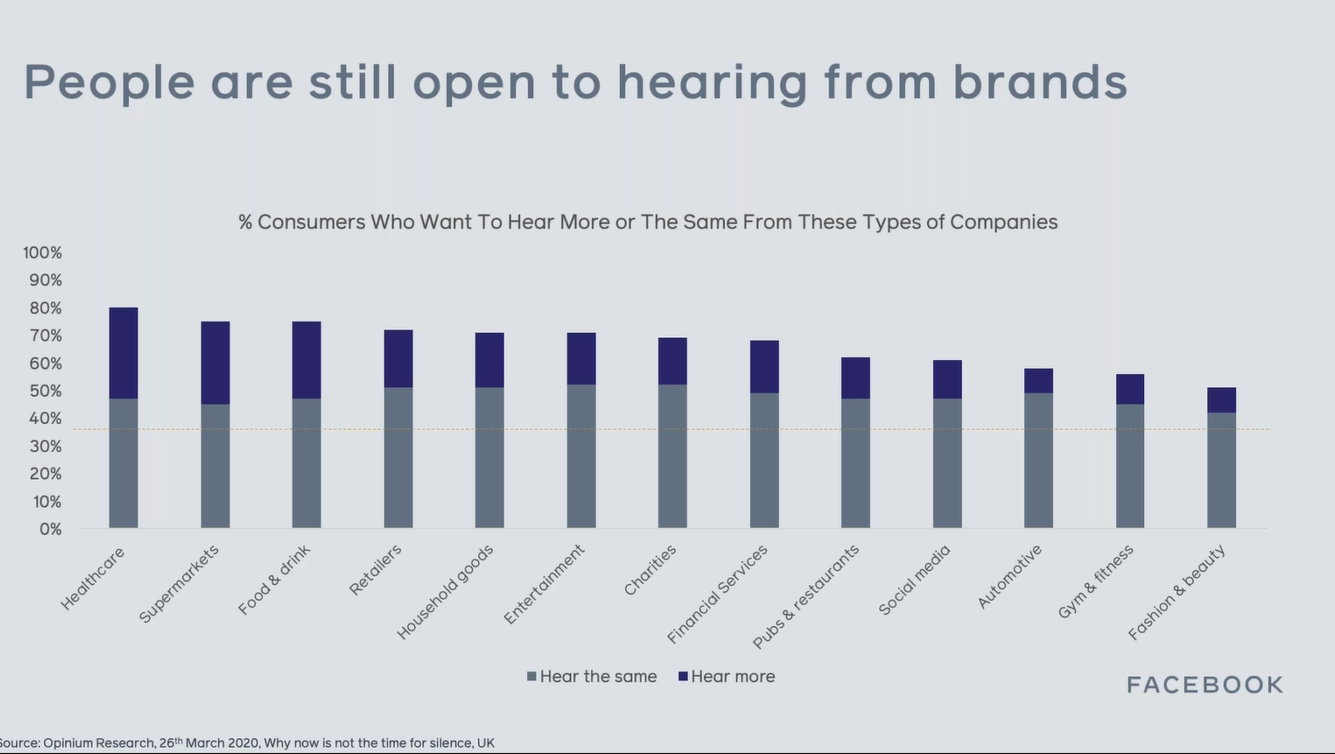

This decrease in fear and increase in boredom is contributing to a shift in attitudes towards advertising. There is a sense that people want to get back to normal as quickly as possible now.

Only 1 in 5 UK consumers currently disprove of brands running ‘normal’ advertising, and across multiple verticals it is clear that some people want to hear more from brands!

For those brands who are standing up to be counted, shifts in sentiment and purchase behaviour are already taking effect. Almost a quarter of UK consumers say they have recently tried a new brand because of the innovative or compassionate way that it has reacted to Coronavirus.

However, consumers do not want brands to be putting profit before people, and it is clear that how brands act now could have massive repercussions for how consumers perceive them for years to come. Speaking up is important, but it is crucial that brands say the right thing.

Thank you to Andy and Pete at Facebook for another great session. Missed our previous write ups? Read the summaries of Session 1 and Session 2 on the ROAST blog.