Facebook EMEA’s fourth COVID LIVE Webinar was delivered on Wednesday 15th March. Below are the key insights from the session:

Insight 1: The financial impact is polarised

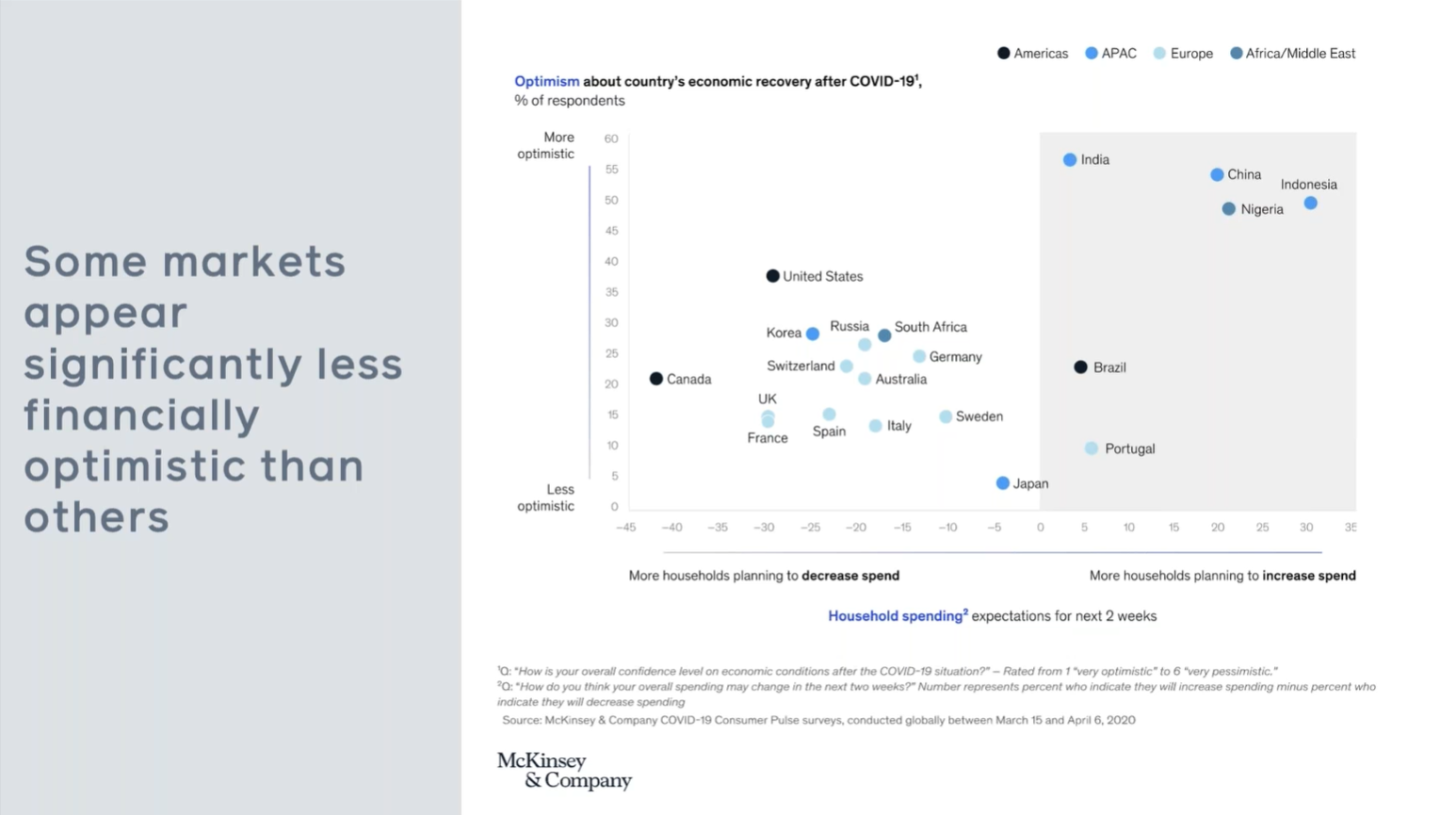

The latest data from McKinsey gives us a global view of economic optimism:

European countries are mainly clustered towards the bottom left because they are currently being hit hardest by the virus, with residents of UK and France saying they are planning to decrease household spend by 30% over the next two weeks. Citizens in countries such as China, who have now (hopefully) seen the back of COVID-19, are planning on increasing their household spend.

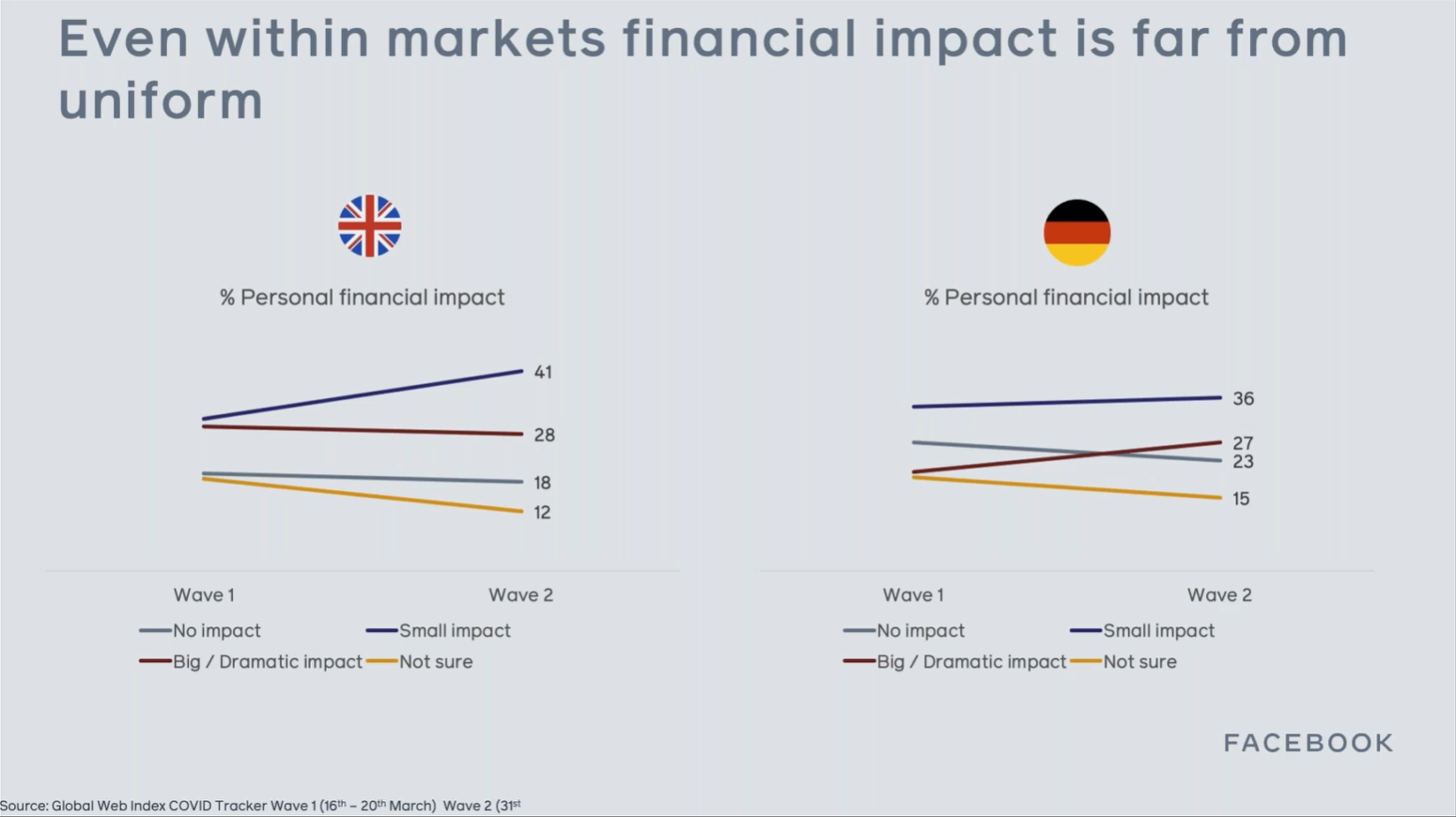

Zooming in on the UK and Germany, we see that the number of people ‘Not sure’ about about the financial impact on them is decreasing:

This suggests that people are starting to see a clearer picture of he real impact it will have on them. The number of UK residents saying it will have a ‘small impact’ on their financials has risen to 41% and the number are saying it will have a dramatic impact has dropped to 28%.

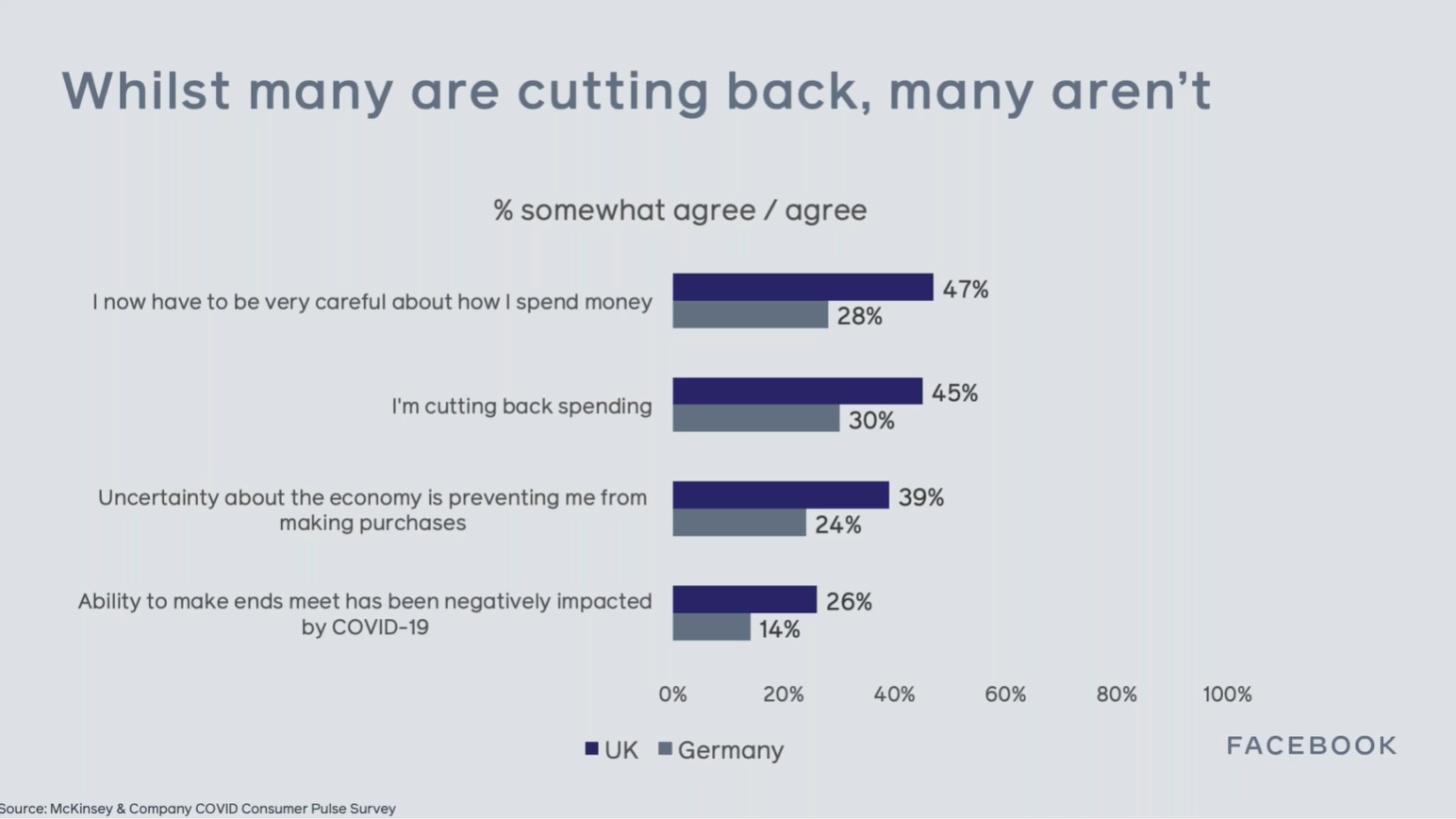

45% of UK residents are now cutting back spending, which is a big percentage, but still a minority.

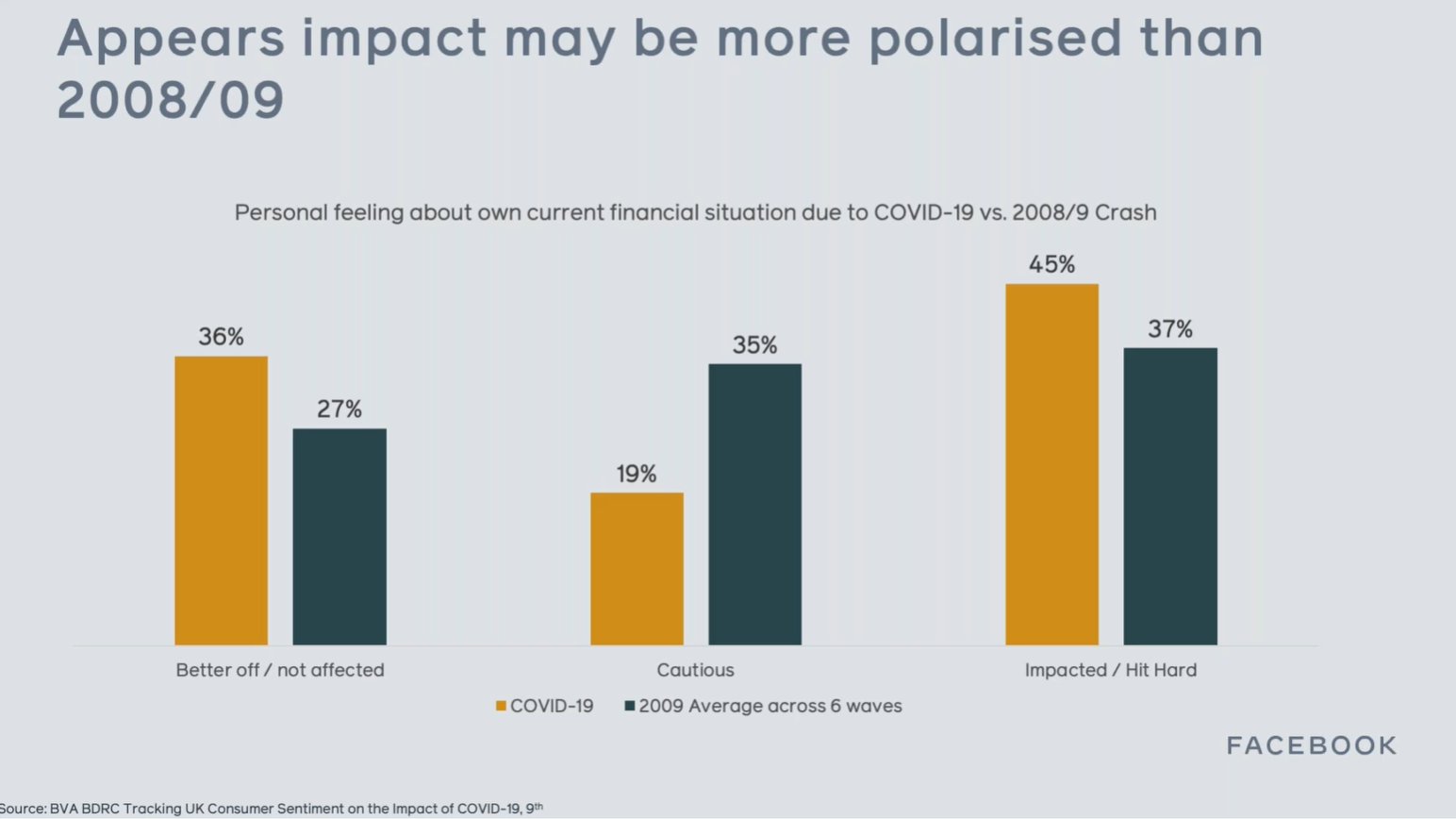

When we compare COVID-19 to the financial crisis of 2008/9, we see how much more polarising the current crisis is proving to be financially. There are more people saying they’ve been hit hard by COVID-19, but also more people saying they are better off or not affected.

Kantar have reported that on average £200 million per week is spent in the UK on eating out, so this is all being saved.

For brands, it’s important to note that not all consumers are poorer. Some who feel like their job is safe and are saving on usual costs like childcare, eating out, transport and holidays, have more disposable income than they are used to.

Are your customers hit hard or unaffected? If they’re in the latter camp, can you lower your prices for them or offer more flexible payment options?

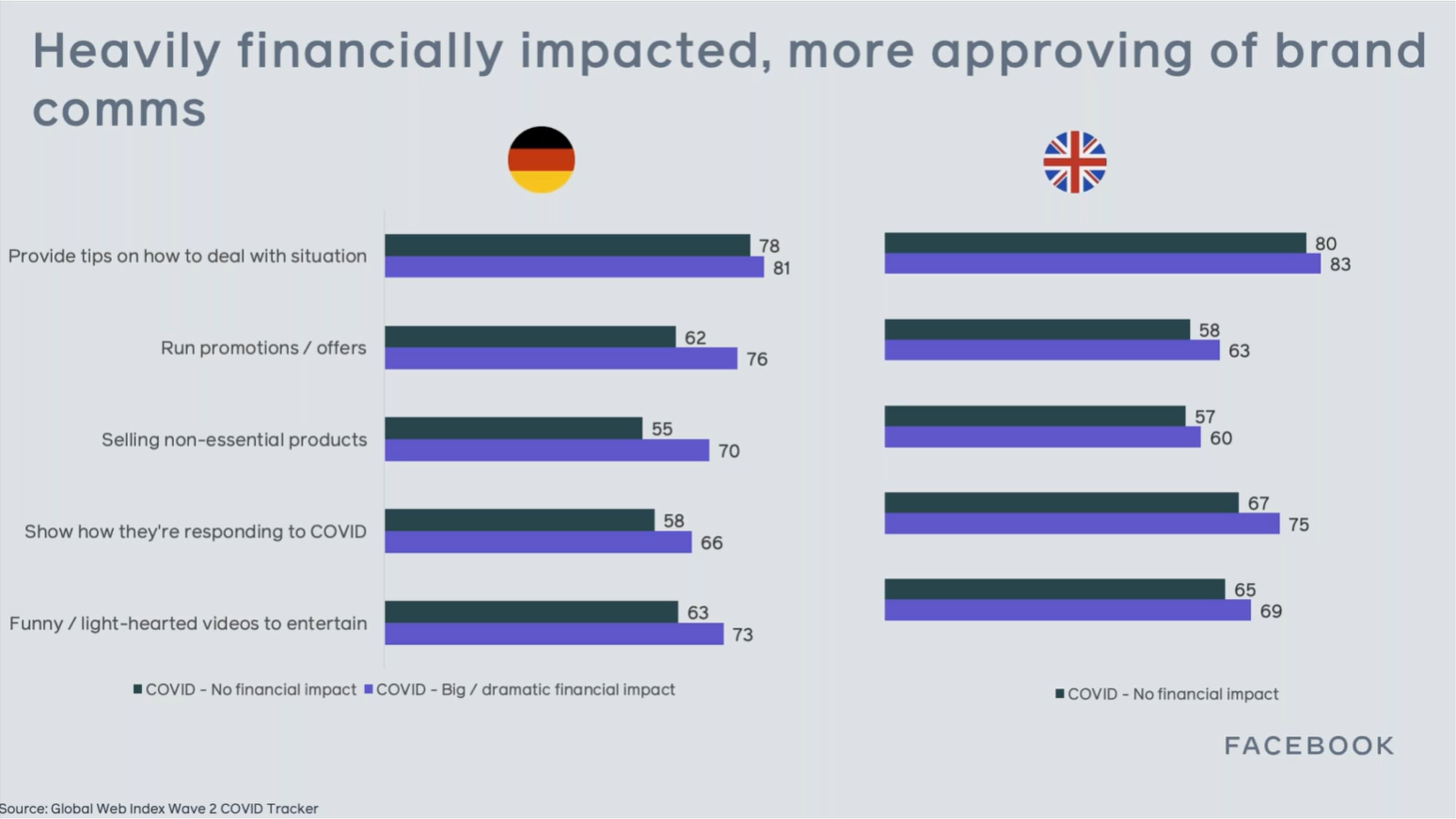

Insight 2: The financially impacted lean-in most to brand communications

Consumers still want to hear from brands, and data from GWI suggests that those who have been dramatically financially effected by COVID-19 are showing the highest demand for brand communications.

In particular, those impacted want funny and lighthearted content more than those who haven’t been affected.

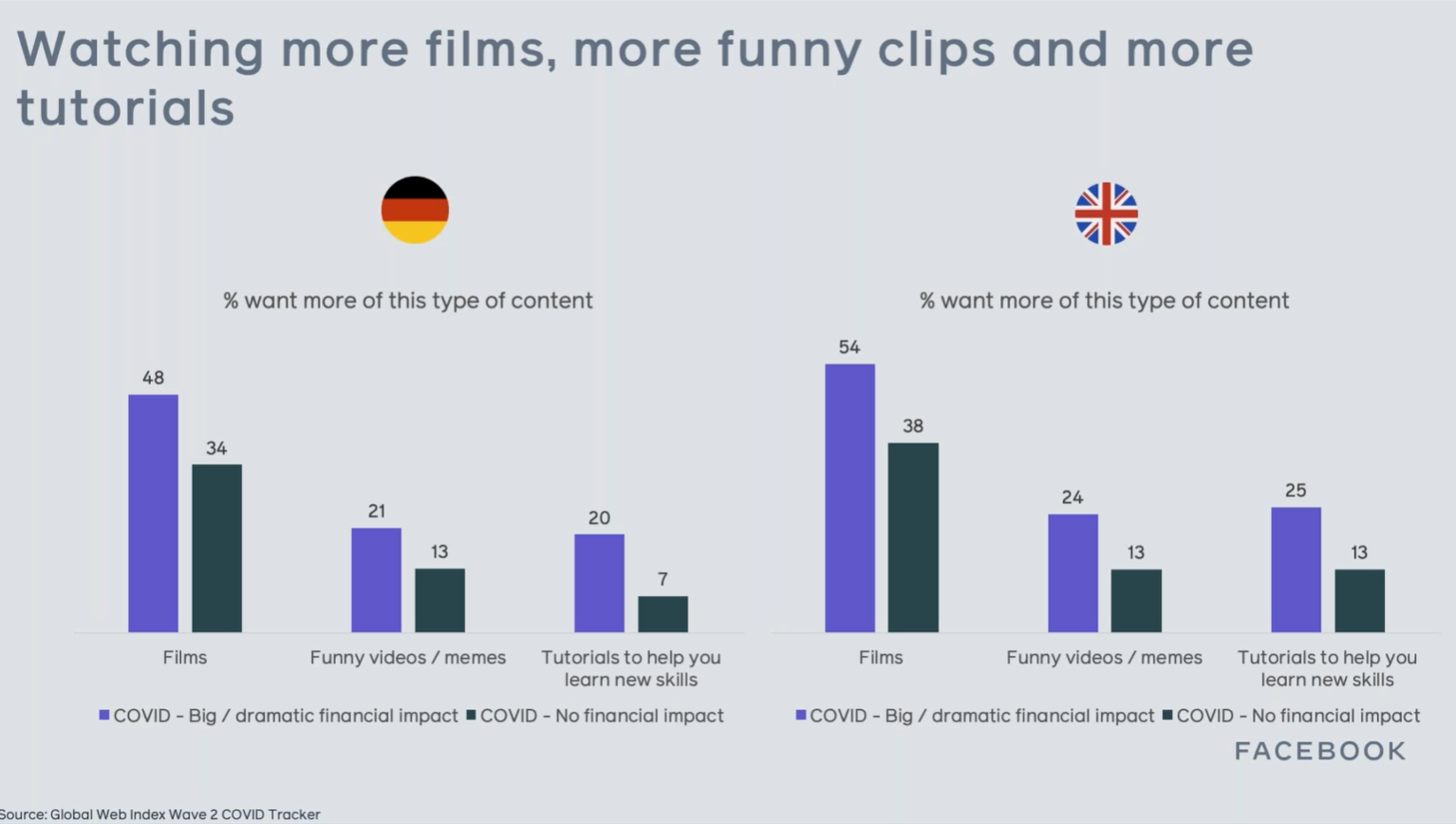

There are two main needs. The first need is to be entertained, which is shown by increased demand for films, funny videos and memes. The second need is to be informed, with those who have been dramatically impacted wanting tips on how to stay healthy along with financial advice.

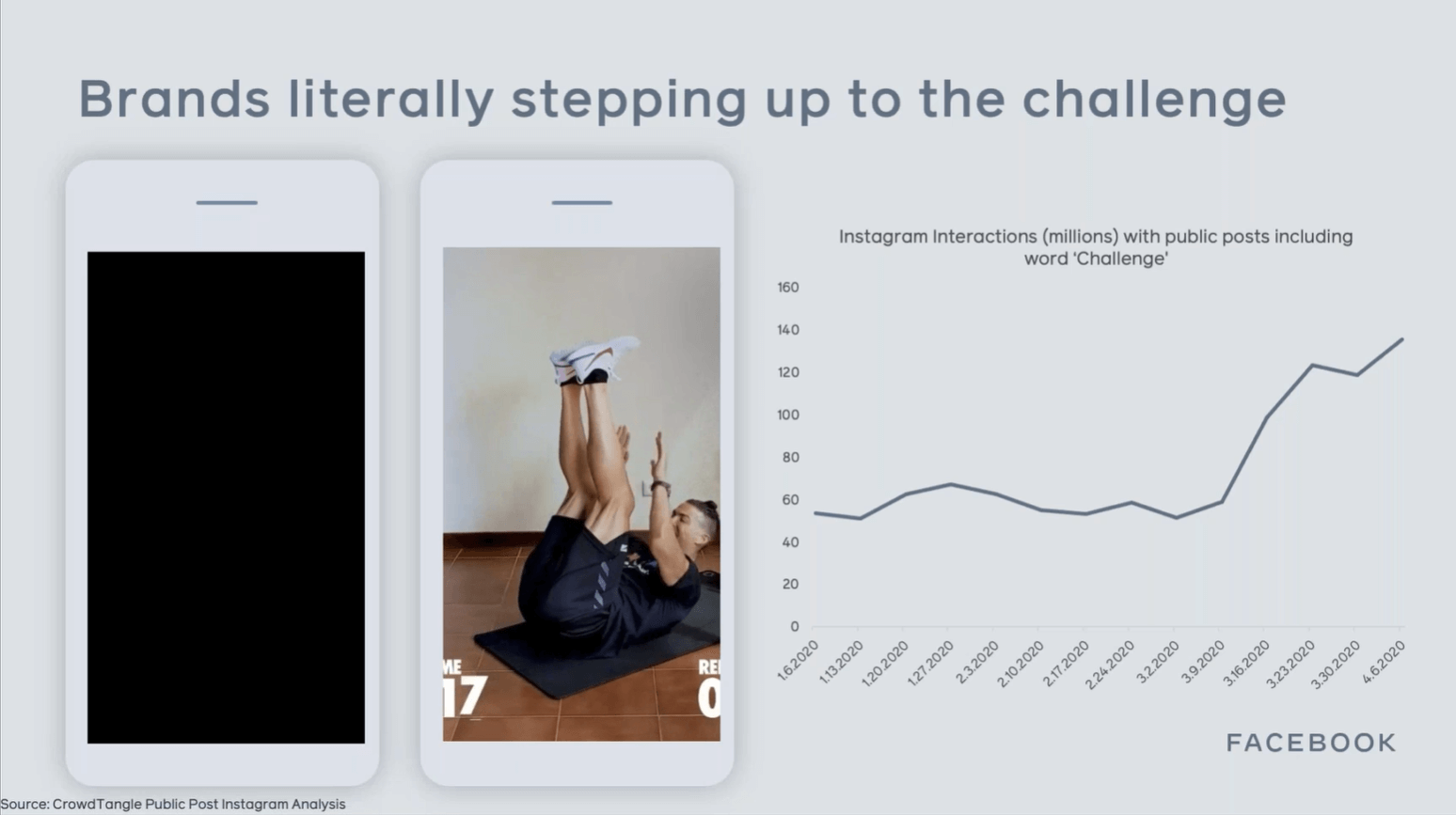

With more time on their hands, people want to be challenged. Charity challenges, such as the Run for Heroes 5K Challenge have exploded on social media (the initial fundraising target was £5,000 and it has now raised £2.5million!). Brands are also getting in on the act, with Nike creating the Living Room World Cup where a pro athlete posts an exercise challenge for people to try to beat at home.

People want brands to be positive and proactive, and Budweiser and Scharwzkopf have been doing exemplary work creating campaigns that will help save small businesses.

The emergence of sites such as Didtheyhelp.com suggests that people will remember how brands behaved during this period of crisis, and brands who stand up to be counted could be seen favourably for years to come.

The question for brands is how are you positioned to help?

What actions have you taken to be more relevant for these polarised audiences?

With a new paper published on Tuesday in academic journal Science suggesting that social distancing may exist in some form until 2022, thinking about this period is no longer strictly short-term.

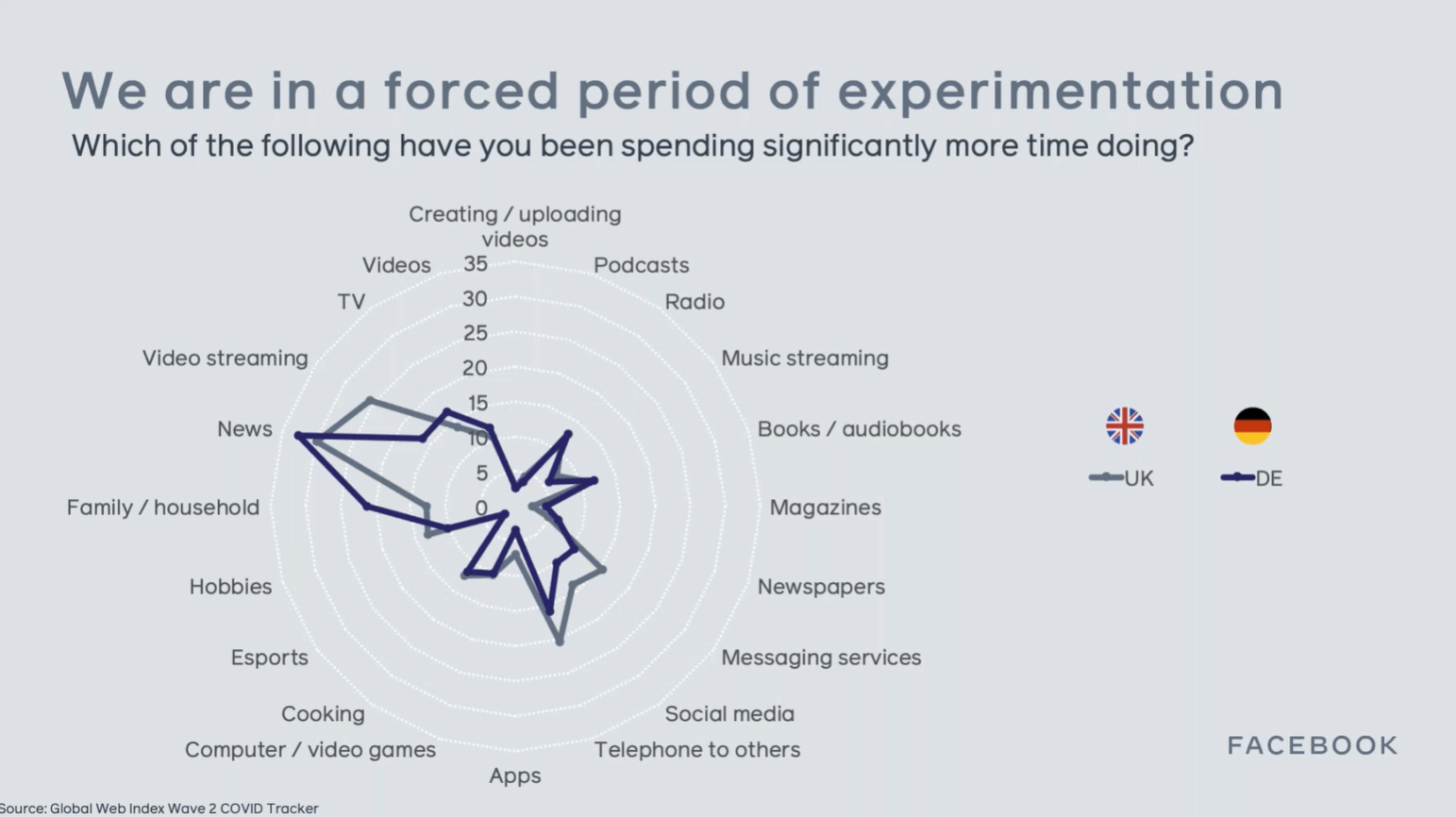

Insight 3: New habits are being formed

In this time of forced experimentation, people are consuming more media than before, and the vast majority of it is online.

Amongst the digitally native 16-24 group these increases are the most pronounced, with increases of 40%+ for streaming and social media usage. But these increases are by no means limited to younger groups, and the 55+ group is showing a big increase in video calling and messaging.

People are being forced into trying out new behaviours, but the real question is which of these will stick after the crisis is over?

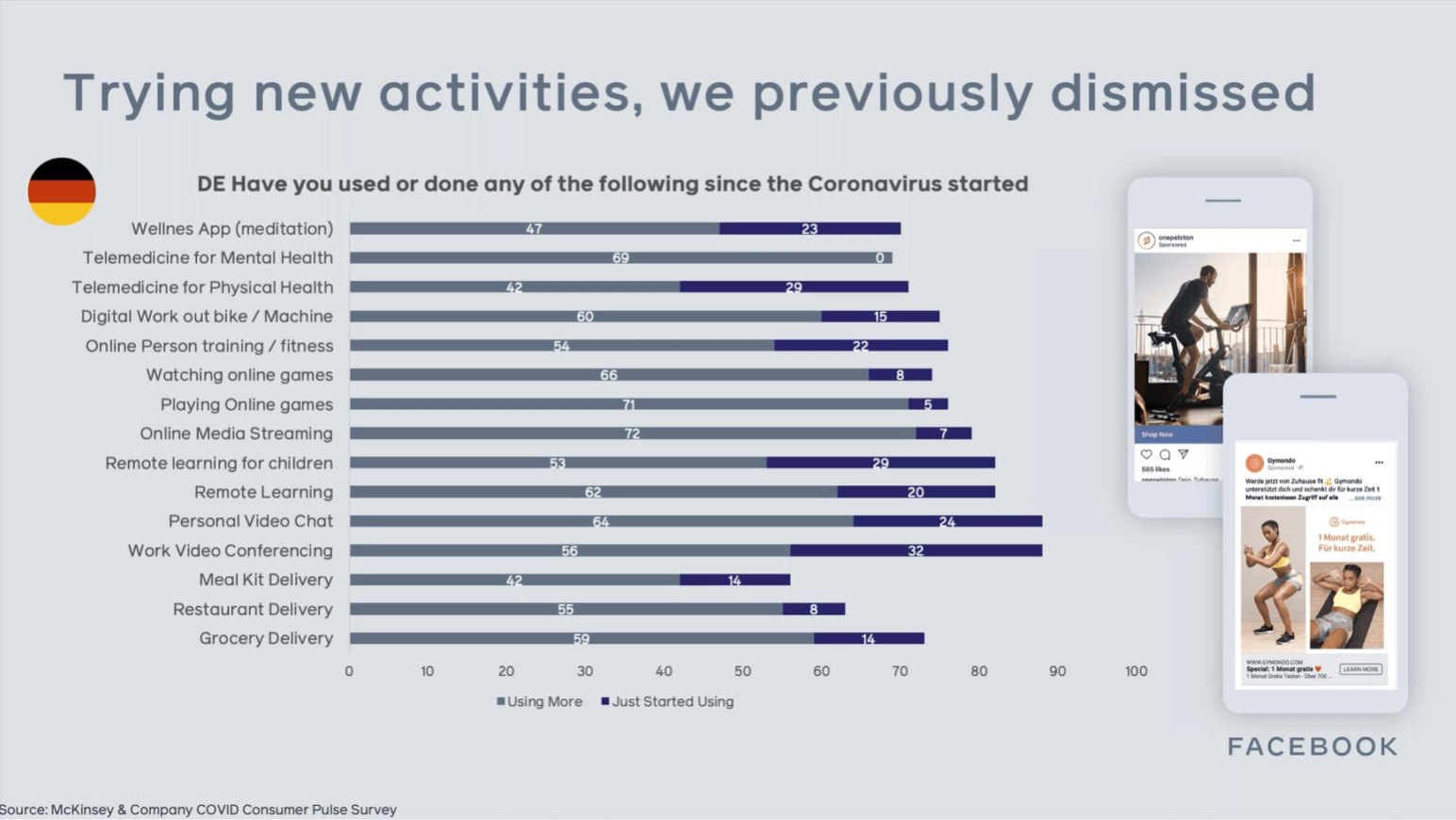

As the gym, the office, the coffee shop, the restaurant and the school all relocate to the home, people trying out virtual and home-delivery services.

Peloton stocks have soared, and they now have now reached 80 million users. Zoom has gone from 10 million to 200 million daily users.

How many of these virtual meetings will return to coffee shops and meeting rooms?

We are going through a vast, forced public experiment, but when it comes to which behaviours will stick and which will disappear, it depends on the nature of the task that is to be done and the experience provided by the replacement.

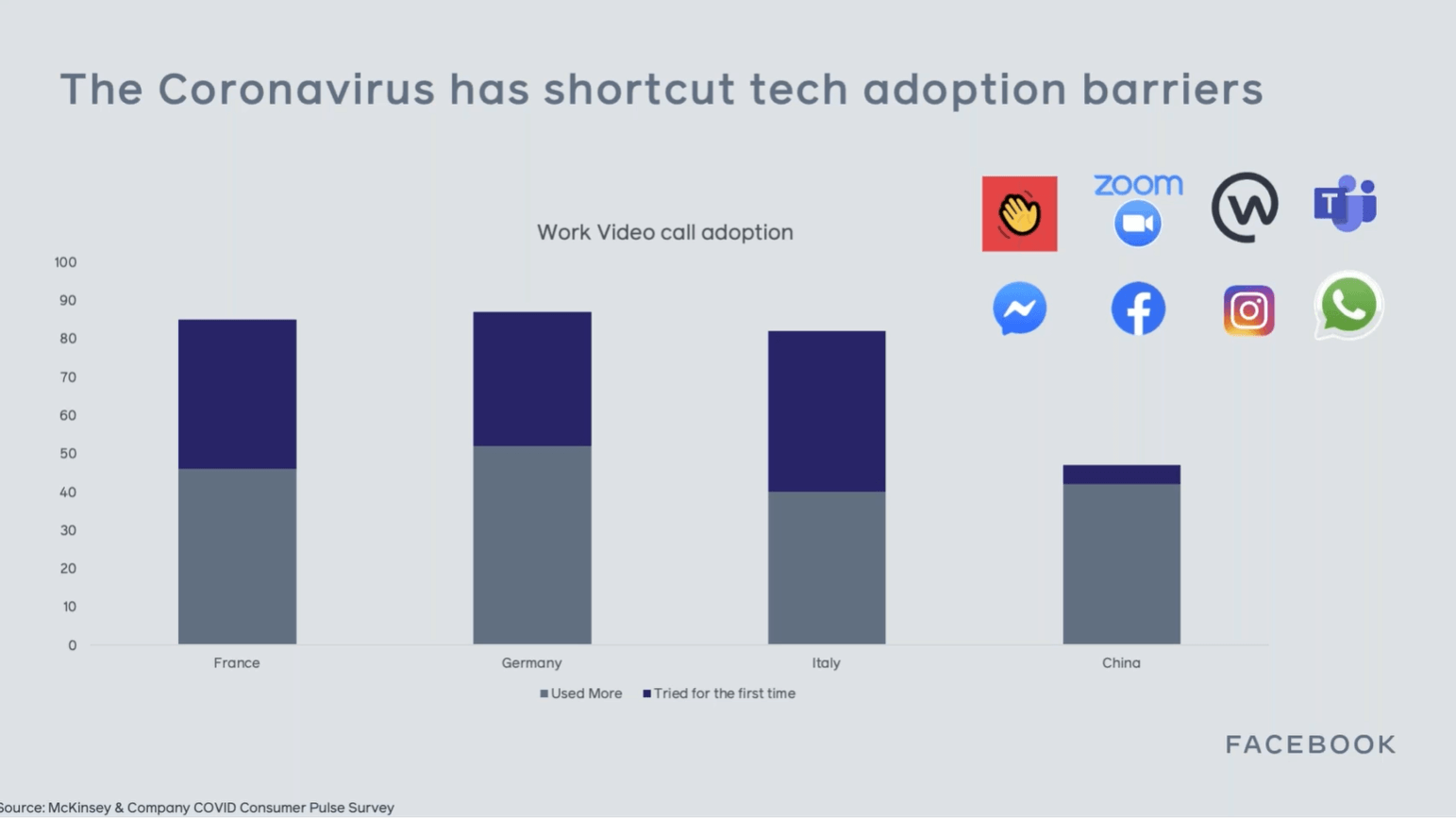

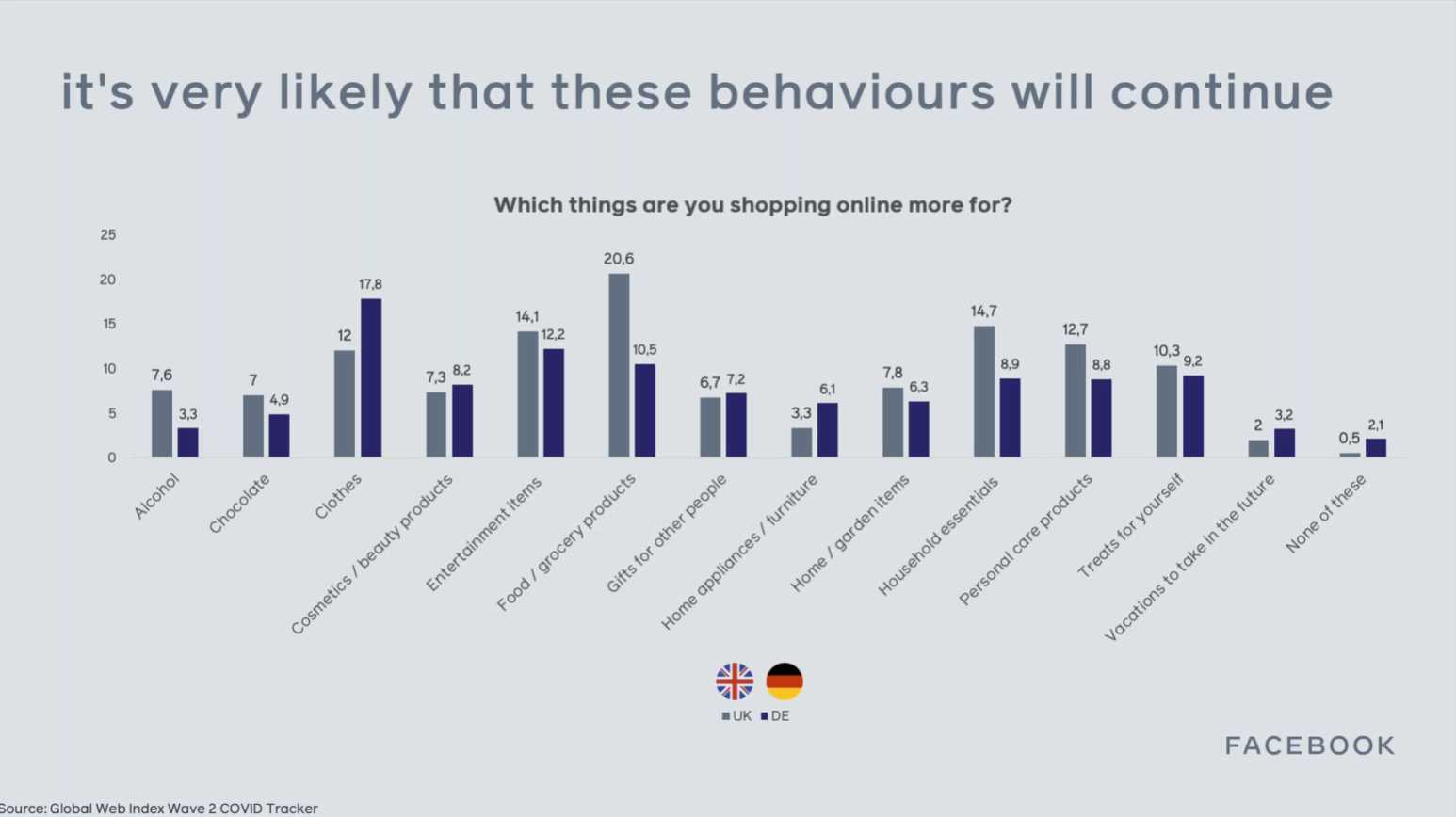

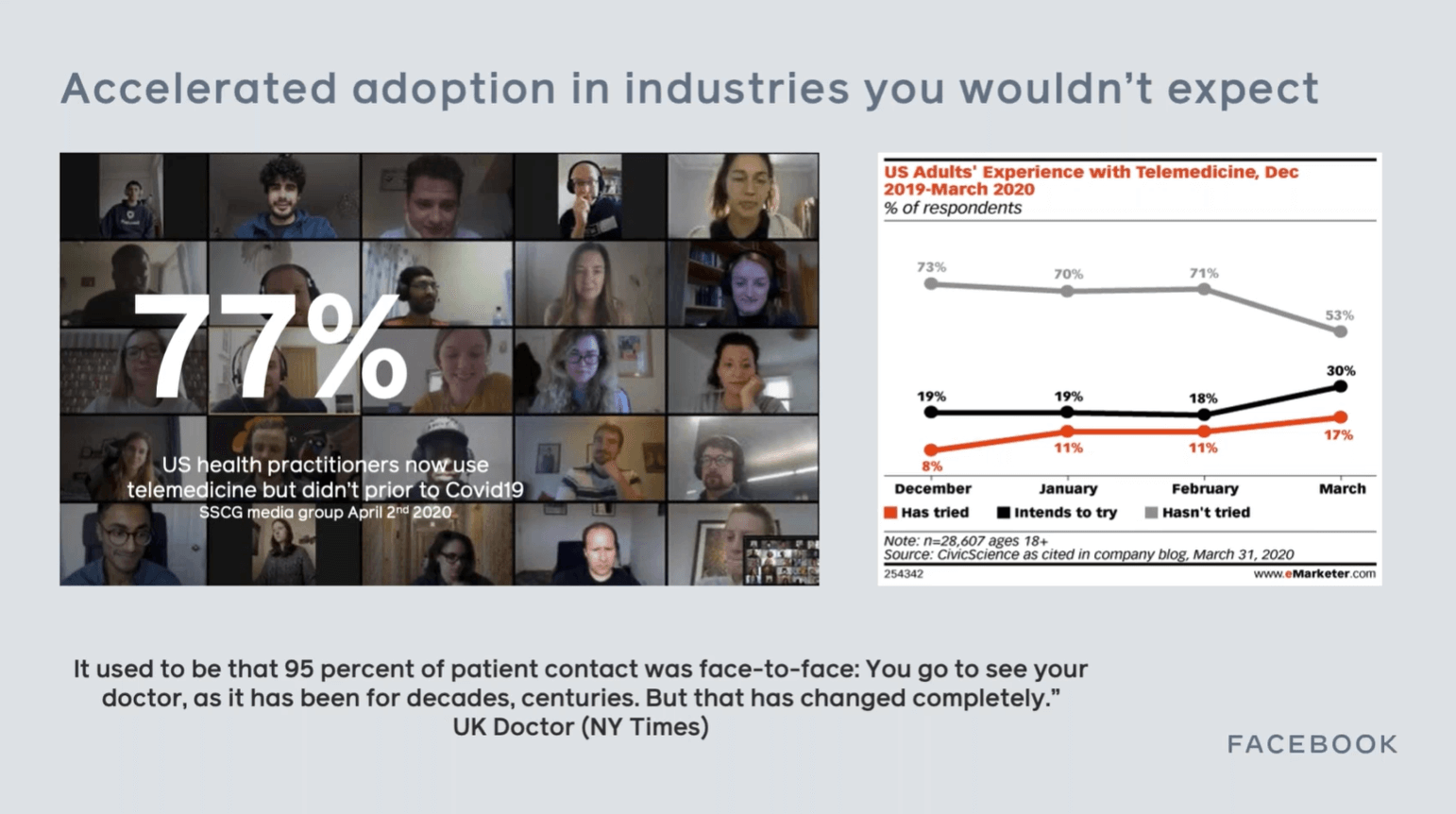

Momentum of buying online is likely to continue, and some industries, such as healthcare, are seeing ancient traditions (face-to-face contact with your doctor) disrupted at a previously unimaginable rate, with 77% of US health practitioners saying they now use telemedicine but didn’t before COVID-19.

Only 1% of UK consultations last year were performed online, but Coronavirus has rapidly accelerated what was a slow digital transformation of a large and change-resistant sector.

Other sectors which have pivoted quickly include fashion, where brands have sent clothes out to models so they can do home photo shoots, and Property with Zoopla reporting a 215% rise in visitors doing virtual viewings.

New habits are being formed and the market is being reset. As we see a decade of change take place in days, we need to keep asking ourselves which of these new habits will stick.

Thanks to the Facebook EMEA team for another informative session.

For more COVID-19 insights, read our summary of last week’s COVID LIVE, or download our whitepaper on The Effects of COVID-19 on Search Behaviour